GoDaddy has lost nearly two-thirds of its market value. Wix has lost almost 90%. The prevailing narrative is that AI is eating the hosting business alive. The numbers, however, tell a far more nuanced story.

Four of my friends made their first exit in the web hosting industry.

Eneko Knörr founded Hostalia. Josean Paunero launched Hostinet. Yago Arbeloa created Sync Entertainment. And Faustino Jiménez founded RapidSite, which eventually became Acens—the very company to which Eneko would sell Hostalia years later.

Faustino didn't stop there. While Eneko was selling Hostalia to Acens in 2007, Faustino was already running Arsys, which acquired Yago's company, Sync, in 2011. In 2013, Arsys itself was sold to 1&1, the German group we now know as IONOS. Meanwhile, Josean sold Hostinet to Total Webhosting Solutions (TWS), the Dutch consolidator that was already beginning to acquire virtually every hosting company it could find across Europe.

Hosting has always been a cash cow. And like every cash cow, it attracted anyone who wanted to milk it.

The first wave of consolidation in Spain was led by Arsys and Acens. They acquired smaller hosting providers one after another until they controlled a significant share of the shared hosting and domain registration market. By the time IONOS acquired Arsys in 2013, the pattern was already clear: the hosting industry wasn't growing organically alone—it was growing through acquisitions. A classic buy-and-build strategy.

The second wave came from abroad.

Netherlands-based Total Webhosting Solutions (TWS) began acquiring hosting providers across Europe, including many in Spain. Gigas, which went public on Spain's MAB market in 2015 with a €14 million valuation, initially expanded by buying smaller hosting companies. Team.blue, backed by private equity, followed exactly the same playbook on a continental scale—and continues to do so today. Sweden's Miss Group has completed more than 25 acquisitions and now operates around 30 brands across Sweden, Norway, Finland, Switzerland, the UK, the US, Canada and Spain, where it acquired ProfesionalHosting and Sered. Grupo Aire, backed by Ardian, has built a converged cloud and telecom operator through the acquisitions of Stackscale, Teradisk, IdecNet and SysAdminOK. I know that last transaction firsthand: at Bondo, we advised the shareholders of SysAdminOK on its sale.

The pattern has repeated itself for two decades, even if the names have changed. A hosting company—almost always backed by private equity—acquires a smaller player, adds its recurring customer base, improves margins, and repeats the process.

If you were a small hosting company generating more than €1 million in recurring annual revenue, you were constantly receiving M&A approaches.

Those who haven't sold their hosting businesses over the past decade haven't done so for lack of offers. They've simply spent years saying no. The best example is Dinahosting. Founded in 2001 and still owned by its original three partners, it generated €15.5 million in revenue and €3 million in pre-tax profit in 2024, compared with €14.2 million and €2.2 million respectively in 2023 (according to Spain's Commercial Registry). It has been turning down acquisition offers for so long that nobody can quite remember when it started.

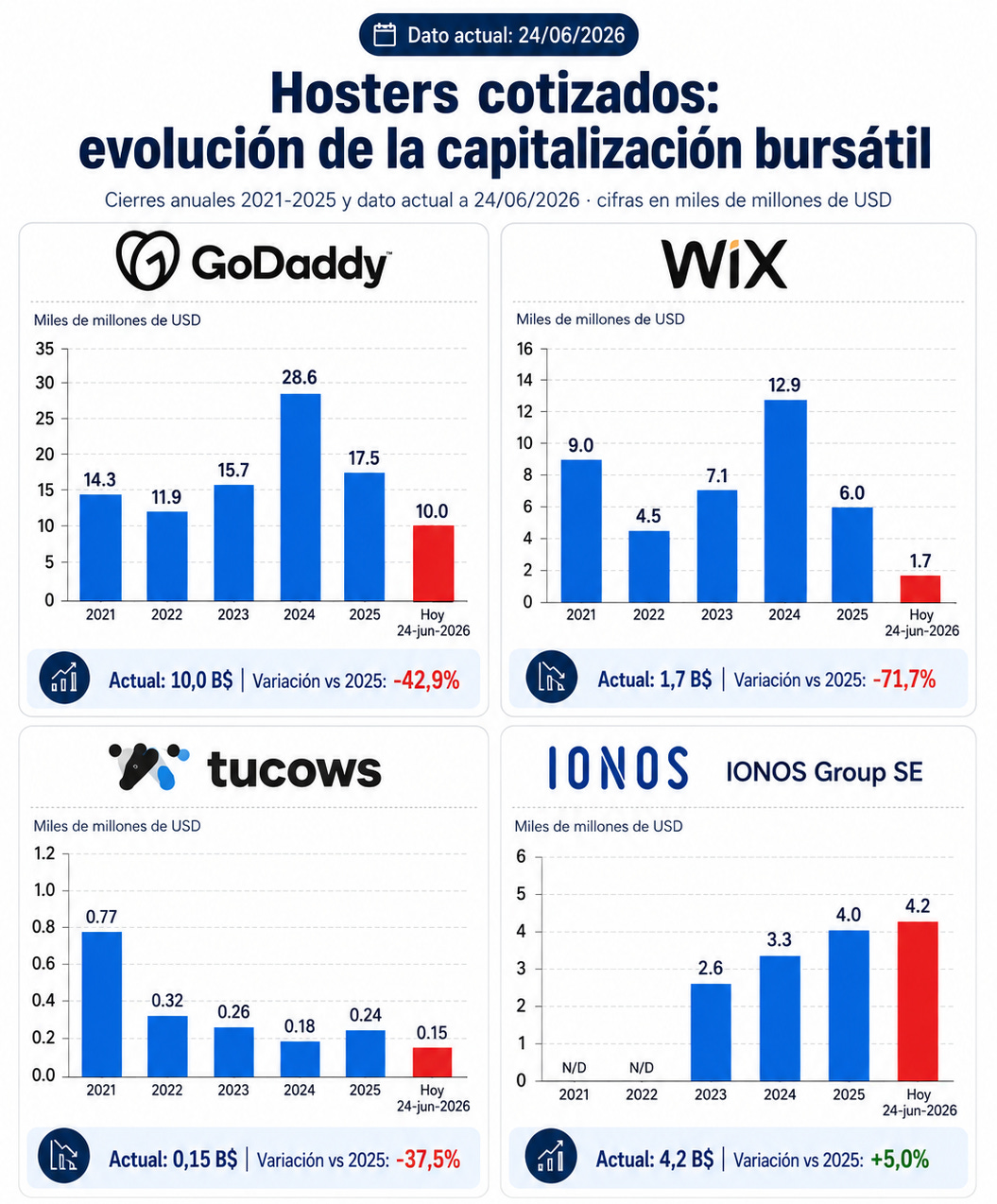

This year, there's been plenty of talk about M&A activity in web hosting slowing down and valuations collapsing. Before discussing whether that's really true, it's worth looking at what public markets have done to four listed companies: US-based GoDaddy and Tucows, Israel's Wix, and Germany's IONOS.

GoDaddy's market capitalization has fallen from $28.6 billion at the end of 2024 to around $10 billion today. Wix has suffered the steepest decline, dropping from $12.9 billion to just $1.7 billion—more than an 87% decline in barely eighteen months. Tucows, which was already trading at relatively modest valuations, has continued to fall and is now worth only around $150 million.

IONOS is the only exception. Its market capitalization has continued to grow year after year, reaching around €4.2 billion today. But annual closing prices don't tell the whole story. IONOS shares peaked at €42 in September 2025 and now trade at around €27—a decline of more than 35% from that high.

This isn't just a hosting story. To a large extent, it coincides with what many have called the SaaS apocalypse—a broad correction in software valuations that has hit hardest those companies where investors see the greatest risk of AI hollowing out the business from within.

That's where Wix has taken the biggest hit, for a fairly obvious reason. Its entire business model was built around attracting people who needed a website builder and pre-designed templates. That was the value proposition. And that's precisely the layer that generative AI commoditizes first. Today, anyone can generate a custom website from a single prompt without ever touching a template.

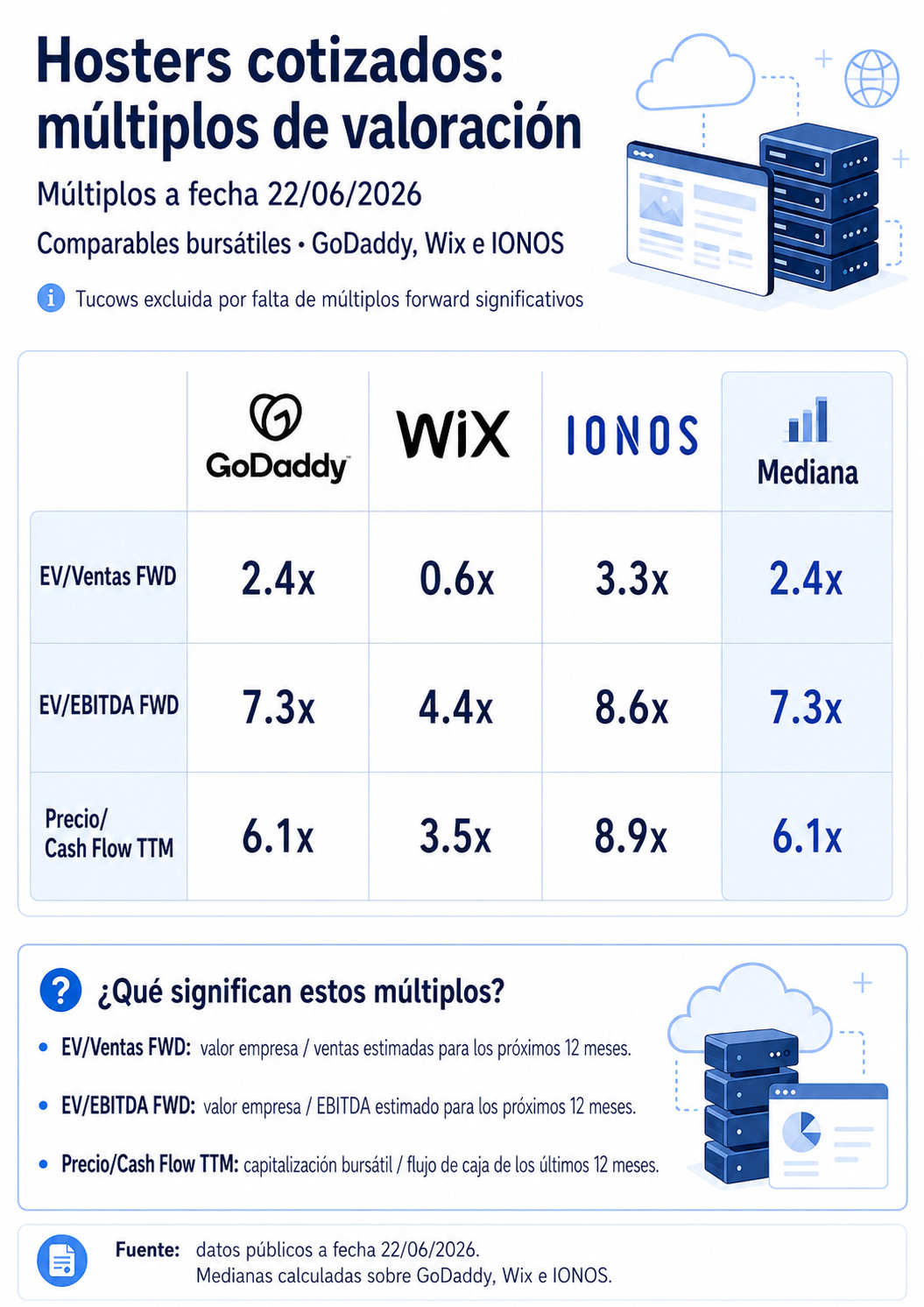

The market is pricing that risk accordingly. Wix trades at roughly 0.6x forward revenue, compared with 2.4x for GoDaddy and 3.3x for IONOS. The median across the three (excluding Tucows, which has very limited forward estimates available) stands at 2.4x revenue, 7.3x EBITDA, and 6.1x trailing twelve-month operating cash flow. Wix trades below that median on every single multiple, without exception.

The numbers, at least for now, don't support the apocalypse narrative.

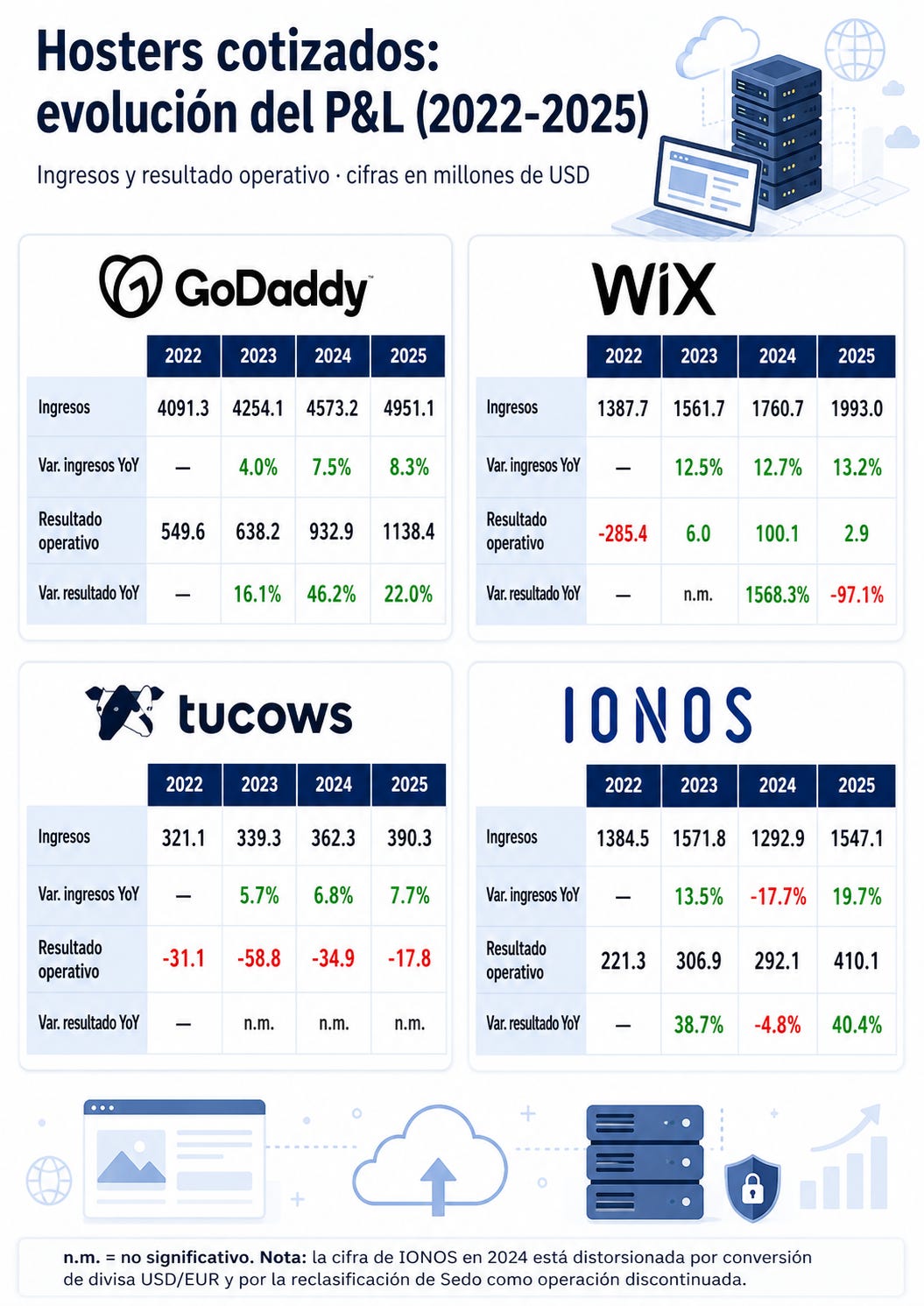

GoDaddy has posted operating profit growth for three consecutive years: 16% in 2023, 46% in 2024, and 22% in 2025, while revenue growth accelerated from 4% to 8.3% over the same period. The trend has continued into Q1 2026, with revenue reaching $1.27 billion, up 6% year over year, and an adjusted operating margin of 24.5%—seven percentage points higher than in the first quarter of 2025.

IONOS reported 7.6% revenue growth at constant currency, added 180,000 net customers during the quarter, and reaffirmed its full-year guidance.

Wix accelerated even further, with revenue 14% higher than in Q1 2025 and annual recurring revenue now exceeding $1.9 billion.

Tucows remains loss-making, but the headline numbers require context. Its losses are largely driven by its investment in fiber broadband through Ting, not by deterioration in its domains business.

Some of this growth has been inorganic, and that's important to acknowledge. But the overall direction of the numbers is unmistakable.

The only figure that deserves closer attention is GoDaddy's slight slowdown in revenue growth during Q1 2026, from 8.3% to 6%. It's far too early to read that as a warning sign, but it is the first crack worth watching. If that trend accelerates over the coming quarters, we may finally be able to say that investors' fears about AI are beginning to show up in the income statement.

For now, however, these companies remain cash-generating machines, continuing to grow revenue and—in the case of GoDaddy and IONOS—expanding margins as well.

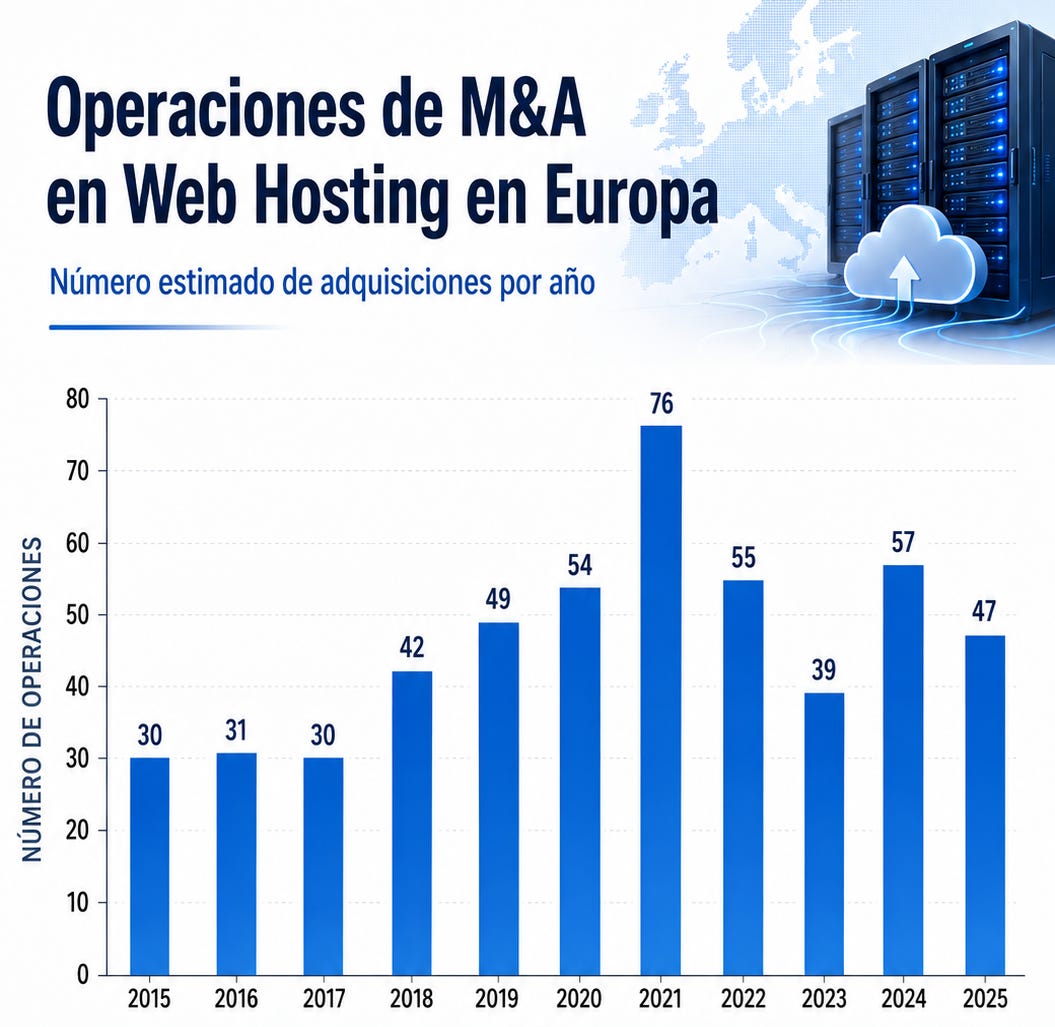

The number of deals peaked in 2021 and still hasn’t fully recovered.

I don’t yet have a clear picture of what’s happening in 2026 in European web hosting M&A. But throughout last year, activity in Europe was still significant. The number of transactions rose from 30 in 2015 to a peak of 76 in 2021, more than doubling in just six years. Then came the decline, down to 39 deals in 2023, the worst year since 2017. In 2024 there was a rebound to 57 transactions, only to fall again to 47 in 2025.

Forty-seven deals is still well above the 30 recorded in 2015, so this is not a story of a market that has disappeared. But it is also not a story of a return to normal either. Since the 2021 peak, there has been no steady recovery—just a sharp drop, a partial bounce, and another decline.

On the other hand, after two decades of consolidation, the issue is no longer a lack of buyer appetite. The issue is that consolidation itself has been so aggressive that there is not much left to acquire. Each wave of deals has wiped out the mid-sized hosting providers with meaningful recurring revenue, leaving either very small operators that are too small to justify a transaction, or the few large independents who, like Dinahosting, have spent years refusing to sell.

If listed hosting companies are under pressure and M&A no longer shows the upward trajectory it had for years, there is an underlying narrative that closely mirrors the broader SaaS story. The idea is that customers are about to migrate en masse from legacy web hosting providers to a new generation of solutions, and that this shift will leave incumbents with a shrinking customer base and little ability to acquire new users.

To understand this narrative, we first need to understand what exactly is supposedly becoming obsolete.

Traditional hosting has historically been split into two broad categories. On one side, specialized hosting providers built around a specific platform—most notably WordPress, but also Drupal, Joomla, and e-commerce systems like PrestaShop or Magento. On the other, generalist hosting companies that built their own template-based website builders—the Wix model—where users select a template, fill it in, and publish without writing a single line of code.

Both models share a structural core: domain registration and hosting. For two decades, this has been the anchor keeping customers locked in and paying month after month with very low churn.

In recent years, larger companies have reinforced this core offering in order to increase average revenue per customer and make switching more difficult. Much of this expansion has come through acquisitions: email marketing tools, analytics, payment solutions, digital marketing suites—all layered on top of hosting to turn it into an ecosystem rather than a standalone server.

The migration narrative argues that all of this—WordPress, templates, CMS platforms in general—becomes obsolete because tools like Claude Code or Codex can now generate entire websites from a prompt, and more importantly, modify them with a level of flexibility that traditional CMS platforms cannot match. A CMS constrains users within pre-built templates. A prompt does not: you simply describe what you want, and it is built for you.

I say this from experience. When I started building my own app with Claude (it is still somewhat surreal that someone with a philosophy background can now build reasonably sophisticated apps through vibe coding), the first suggestion the system made was to deploy it on GitHub and Vercel.

Vercel has effectively become the default destination for any AI tool generating a website or application, which has helped push its valuation to around $9.3 billion. Around it, a new ecosystem has emerged—companies that did not exist in their current form three years ago and are already operating at meaningful scale. Lovable has surpassed $500 million in ARR. Framer raised $100 million in August 2025 at a $2 billion valuation, with ARR expected to approach $100 million by end-2026. None of these companies existed in their current form more than a few years ago, and together they already represent over $20 billion in combined valuation.

The funnel that companies like GoDaddy and Wix have monetized for two decades—domain, hosting plan, template—is collapsing into a prompt. You describe what you want, and the website is deployed. Pricing is no longer about features; it is about cents. A $20/month Claude subscription can now generate custom websites that would have cost thousands of euros just a few years ago, compared with €13.99/month for Hostinger AI or $17 for Wix’s entry-level plan.

That said, the key question is timing, not direction.

For a website that has been running for five years and is only updated once a year, none of this matters yet. That customer has no urgency to rebuild anything, and as long as nothing is rebuilt, they continue paying exactly the same bill. Most SMEs are in the same situation: they are unlikely to start vibe-coding their own websites anytime soon, and will probably continue hiring someone to build and maintain them.

Large hosting companies, which have the resources to adapt, are already moving—each at their own pace. GoDaddy has developed Airo, its own AI-powered builder, which so far is generating relatively modest revenue—around $10 million annualized. Wix acquired Base44 for $80 million in June 2025; the platform’s ARR grew from $3 million at the time of acquisition to $150 million just eleven months later. Team.blue, the European consolidator that has been buying traditional hosting companies for over a decade, made a similar move in December 2025 with Macaly, another vibe-coding platform.

The problem sits lower down the stack. A small hosting provider does not have the resources to build a competitive AI layer or acquire a vibe-coding startup, nor will it be the default hosting option suggested by tools like Codex or Claude Code—that position is already occupied by Vercel. This makes it significantly harder to acquire new customers, even if churn among existing customers remains low, since those users are precisely the least likely to migrate.

For mid-sized hosting companies without a clear strategy for competing in this new environment, the most rational short- to medium-term decision is probably not to go it alone, but to consolidate into a larger platform.

The good news is that, even if the M&A market is far less active than in 2021, these businesses remain highly valuable assets. Most still have large and diversified customer bases, low churn driven by the stickiness of domain anchoring, and extremely strong cash conversion—often close to 100% EBITDA-to-cash flow—typical of prepaid subscription models.

This asset base will continue to be attractive, especially for larger players that are shifting toward AI-enabled platforms but still want access to a broad installed customer base. New companies will emerge and some migration will happen, yes, but a very large share of businesses is still on legacy platforms and will remain there for years. The fastest way to acquire that base is not to build it customer by customer, but to buy it—with all the cash flow that comes with it.

And right now, the new cash cow attracting capital at a pace the traditional hosting industry never saw is data centers. But that is a story for another article…

Over the past few years, I’ve published hundreds of posts, articles, and infographics about M&A on LinkedIn.

Some friends had been telling me for a while that I should do more video content and open an Instagram account.

The truth is, I’ve never been comfortable in front of a camera. It has always felt slightly awkward (to put it mildly).

But there comes a point where you stop making excuses.

So I’ve finally decided to take the plunge and set up a public Instagram account, where I’ll be sharing short videos about buying and selling companies.

If you’d like to follow along, you can find me here:Instagram profile

Joshua Novick, Managing Partner at Bondo Advisors.

cloud technology axon

During Portobello’s ownership, the business grew revenues organicall...