Bondo publishes its M&A Report on IT Consulting in Iberia and Europe

At Bondo Advisors, we have just released our new M&A Report on IT Consulting in Iberia and Europe.

(Download the report here: https://bondoadvisors.com/informe-it-consulting )

By analyzing more than 200 recent transactions and the evolution of valuation multiples across the sector, several clear conclusions emerge regarding valuations, market dynamics, and industry consolidation.

The performance of publicly listed IT consulting firms in Europe shows how the market has gradually normalized multiples after the 2021 peak. Today, valuation levels are much closer to historical averages: around 1x revenue and approximately 10x EBITDA at the median.

Valuation Multiples in IT Consulting

If we look at private transactions, especially in smaller companies, the pattern is very similar. For deals under €10 million in Enterprise Value, the average multiple is roughly 0.8x revenue and around 9–10x EBITDA.

In practice, about 1x revenue is often a useful benchmark for small consulting firms. This pattern is seen consistently not only in IT consulting, but also in strategy consulting, management consulting, or marketing agencies—businesses where growth is closely linked to team expansion and the billing capacity of the people involved.

M&A Activity in IT Consulting in Europe

The sector continues to show very high M&A activity. After the peak in deals during 2021–2022, the market has stabilized but still records hundreds of transactions per year across Europe.

Another interesting insight is that more than half of the deals involve companies valued under €10 million, reflecting the sector’s still highly fragmented nature. The median deal size also remains relatively low, around €7–10 million, confirming that much of the consolidation is happening through acquisitions of small firms or specialized boutiques.

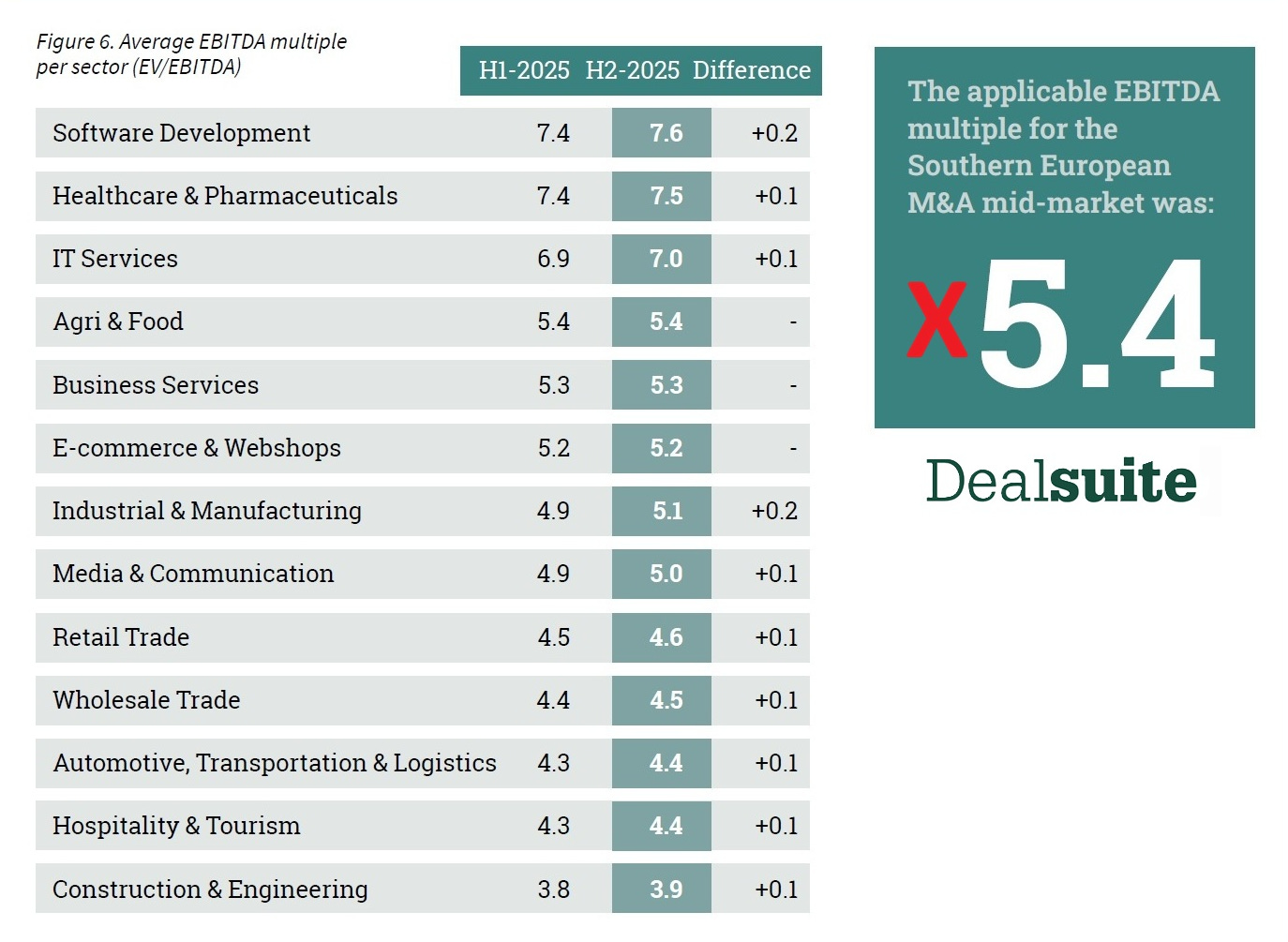

EBITDA Multiples in the Mid-Market of Southern Europe

Another interesting insight comes from the latest Dealsuite M&A Monitor, which analyzes buy-and-sell transactions in the mid-market segment in Spain, Italy, Portugal, and Greece.

The report places the average EV/EBITDA multiple at around 5.4x for mid-sized companies in Southern Europe. Naturally, multiples vary significantly depending on the sector.

According to the study:

In the case of IT services and technology consulting, the average multiple of around 7x EBITDA aligns well with what we observe in our analysis of recent transactions in Iberia. In many deals involving small IT consulting firms, valuations of 9–10x EBITDA are common; however, in many cases, these valuations include earn-outs. That is, an initial price close to 7x EBITDA plus an earn-out can bring the total valuation into the 9–10x range, depending on factors such as growth, specialization, or the quality of the client portfolio.

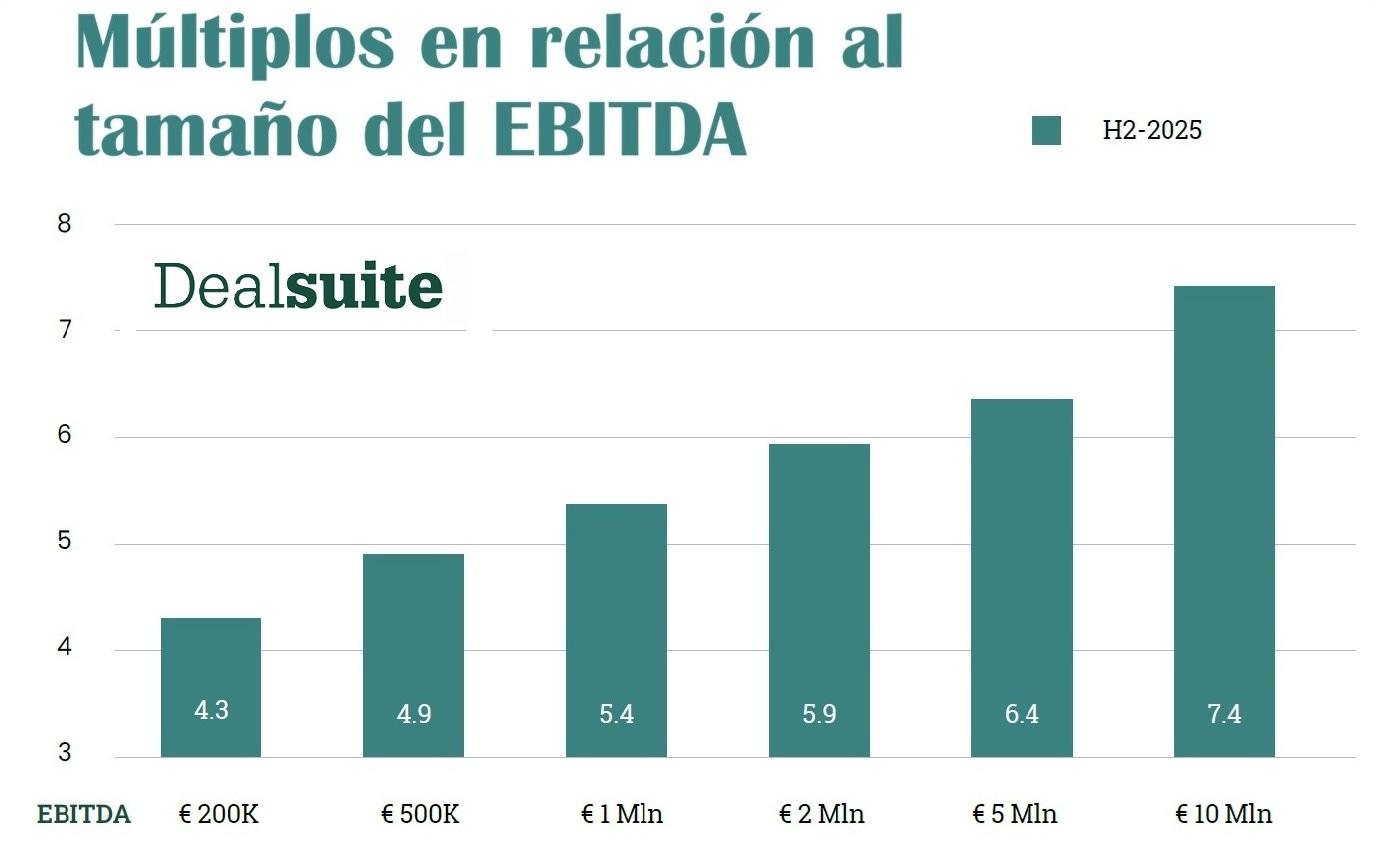

The report also highlights a recurring pattern in M&A: company size has a very strong impact on valuation.

As EBITDA increases, so does the multiple:

This clearly shows that larger, more mature firms command higher multiples, reflecting lower perceived risk and greater strategic value to buyers.

In other words, between a company with €200k EBITDA and one with €10M, there can be a difference of more than 3 EBITDA multiple points. This is why many IT consulting firms aim to grow through acquisitions, as achieving greater scale usually translates directly into higher valuations.

Who is Driving Consolidation in IT

Despite all the debate about how AI could automate part of the technical work, the reality is that demand for technology services continues to grow. Companies are accelerating their digital transformation in areas such as cloud, data, cybersecurity, and artificial intelligence.

However, large clients increasingly prefer to work with consulting firms that can offer a full range of services and specialized profiles. Advanced capabilities—tools, training in new technologies, methodologies, or specialized talent—are usually concentrated in the largest firms.

This is widening the competitive gap between large platforms and smaller consultancies. Many small firms struggle to compete for large projects and specialized talent, which is accelerating sector consolidation.

Larger companies are growing through acquisitions to incorporate talent and capabilities, while many smaller firms are opting to sell. Competing for clients and skilled professionals is becoming increasingly difficult, and remaining a small player in a market increasingly dominated by large platforms is starting to pose a strategic risk.

M&A Report on IT Consulting in Iberia and Europe

Download the full report here:

https://bondoadvisors.com/informe-it-consulting/

cloud technology axon

Addleshaw Goddard (AG), the London-headquartered international law fir...