Founders, KPIs, cross-border deals, and the reality of selling a tech company without falling into the usual mistakes.

How I lived through my first major tech fundraising round and what I learned about advisory in tech M&A

In the early 2000s, I was leading a project I had founded called Demasiado. The formal name was Demasiado Holdings Corporation. Explaining exactly what it was would take quite some time, but in short, we developed and integrated applications like chat, webmail, rings, forums, free hosting, and banner-exchange systems within a portal called Demasiado.com. The idea was to offer these tools to other websites in exchange for managing their advertising inventory through I-Network, our ad network.

We had raised more than ten million dollars from Spanish and Mexican investors, and I was focused on a new thirty-million-dollar round at a post-money valuation of one hundred million. My goal was to secure what at the time was called smart money, especially from U.S. funds.

At that moment, if you wanted to attract investors of that level, you were practically required to work with an investment bank. So I started meeting with several advisors in the market. Very quickly I realized that the generalist banks I spoke with did not understand what we were building. They didn’t grasp the business logic, the technology, or the key metrics. Their approach was to try to fit the project into an existing category by comparing it with large publicly listed companies without digging into the real fundamentals.

The turning point came when a contact introduced me to Alex Brown, a tech-focused boutique that had been acquired by Deutsche Bank to reinforce its push into the digital sector. For the first time, I could explain the technological side without oversimplifying it. They understood the difference between a “hit,” a “page view,” or an ad impression, and we spoke the same language when discussing user metrics, activity, acquisition, or costs.

At that time we were generating around one million dollars a month—and also burning more than half a million, partly due to expansion into new markets. If someone had tried to value the company using an EBITDA multiple, the result would have been ridiculous. An analysis focused solely on the bottom line of the P&L would have led to the conclusion that the company was worth practically nothing. And yet, the value was in the technology we had built, in user growth, in the deals we were closing with other websites, and in the real potential of the project.

The market launch coincided with the dot-com crash, and the round didn’t go through. We ended up selling the Demasiado.com part to EresMas for peanuts, and we separated I-Network, which later became Antevenio—the company we took public on Euronext Growth in Paris and fully exited in 2018.

How we bought companies and why generalist advisors almost never sourced deals

During the years I led Antevenio, we made several acquisitions and received an enormous number of M&A opportunity teasers from banks. Out of the ten acquisitions we eventually completed, only one had been sourced by an advisor. The other nine we found ourselves. In those years, we must have received at least a thousand teasers and easily signed ten NDAs per year. The problem was that many of those companies weren’t relevant to us and were also very poorly explained.

And I’ll never forget a case in which we entered a due-diligence process with a company introduced by an advisor. When we analyzed their data, it became obvious that they had falsified logs and were trying to deceive us. We detected it very quickly, and I always wondered how the bank had not noticed the inconsistencies in the data and KPIs they had sent us. For us, they smelled wrong from the very first moment. And they were.

What I learned then is something I’ve seen repeated many times. The difference between working with a tech-specialized advisor and relying on a generalist bank can be enormous. A generalist may have a strong brand and contacts, but if they don’t understand your sector, your KPIs, or the logic behind the value of your project, the conversation with the buyer or seller starts off on the wrong foot.

That contrast I lived as an entrepreneur is the same one I see today from the advisory side.

Why you need a specialist—not a generalist boutique—in tech M&A

In 2020, when we started Bondo Advisors, we knew we could offer something that didn’t exist in the market. We wanted to build tech-focused M&A advisory led by partners who had created tech companies and led tech teams for years. We didn’t come from learning this sector from the outside. We had lived inside it.

Having been founders and operators allows us to understand very clearly what a founder goes through when they decide to sell their company. We’ve been through sale processes, integrations, earn-outs, new responsibilities within the buyer, and also the moment when you fully leave and have to rebuild your life from scratch.

Five years and more than 20 advised transactions later, our experience reinforces something I already saw as an entrepreneur. In almost any sector, it makes sense to work with a specialist—but in small and mid-sized deals, say between ten and one hundred million, the big banks don’t get involved. Their highly specialized sector teams work on higher-ticket deals.

Those transactions end up in the hands of boutiques. And boutiques, due to their size, can’t have sector-specific teams. One day they’re selling a canned-food company, the next day a steel company, and the day after that an industrial cleaning business. In many sectors that works. If the value depends only on the P&L, the balance sheet, and an EBITDA multiple, you can get by.

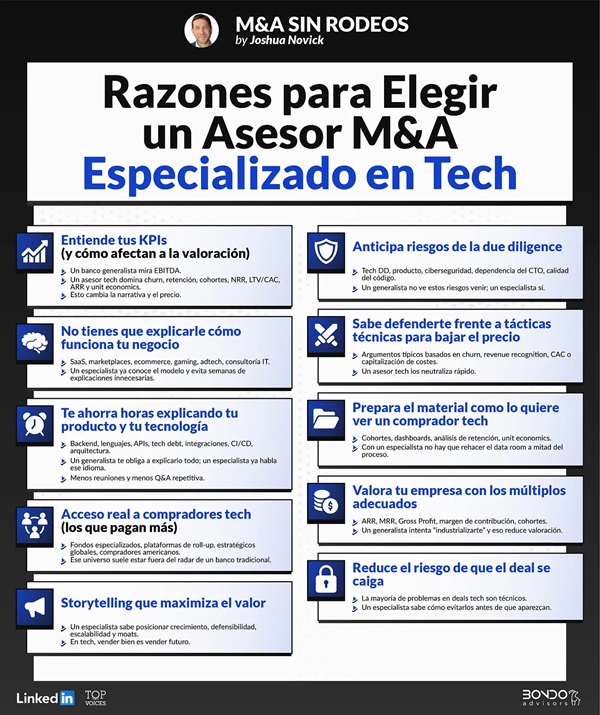

In technology, you can’t. In tech, valuation doesn’t depend only on EBITDA. Investors value retention, NRR, installed base, product, growth, recurrence, technology, cohorts, and scalability. And luckily, it’s a sector with a high volume of deals. After real estate, it’s probably the market with the most annual activity. A tech-focused M&A boutique can specialize and live solely off that.

That’s why generalist advisory—though it may work in other sectors—falls far short in technology.

What a specialized tech M&A boutique provides that no one else does

These are the clearest reasons we see every day, both from my experience as a founder and from what we experience advising software, SaaS, and digital businesses:

In sectors where everything revolves around the P&L, the balance sheet, and an EBITDA multiple, specialization doesn’t change things much. But in technology M&A, it does. The value lies in metrics, product, installed base, retention, technology, recurrence, scalability, unit economics, and more.

If you want a buyer to truly understand all of that, you need someone who speaks your language—like we do.

Don’t hesitate to contact us through the website of our tech-focused M&A boutique, Bondo Advisors, or via my LinkedIn profile.

By Joshua Novick, Partner at Bondo Advisors

Source: https://www.joshuanovick.com/p/como-elegir-asesor-para-vender-tu

cloud technology axon

Addleshaw Goddard (AG), the London-headquartered international law fir...