About ten days ago, when I read the figures for the acquisition of Fotocasa and Habitaclia by Scout24, I was surprised: €153 million.

A number that is certainly not small (I would have loved to receive that when I sold my company), but of course, I kept in mind the €2.925 billion that Cinven paid for Idealista, and at first glance, the price seemed low.

I had always mistakenly thought that Fotocasa and Habitaclia were more or less on par with Idealista. Yes, I knew Idealista was the clear leader and had expanded internationally, but I never imagined that the difference in size, revenue, and EBITDA was so large.

So I went back to review the press releases for both transactions and found these figures:

The valuation reflects this gap:

If Fotocasa/Habitaclia had been valued at the same revenue multiple as Idealista, the price would have been close to €600 million. And I am sure Adevinta, the seller, would have loved that.

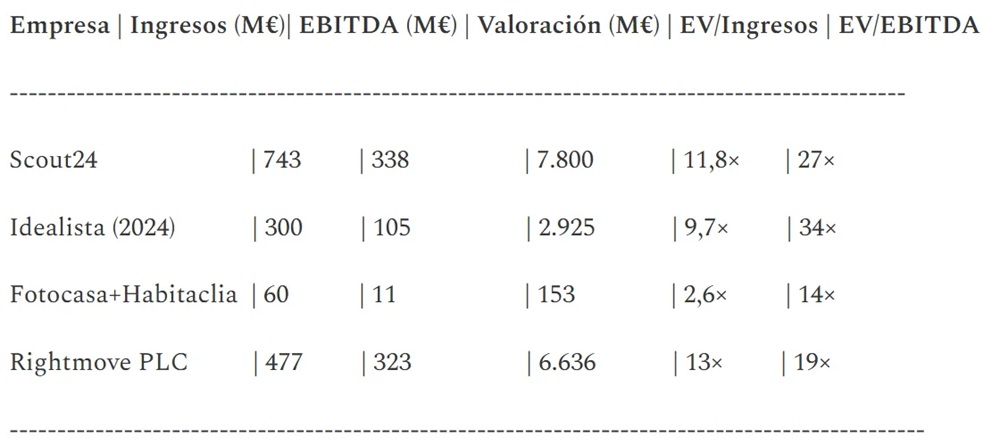

To put this in perspective, here is a comparison of Idealista and Fotocasa with their two European peers: Scout24 (the buyer, listed on the Xetra stock exchange) and Rightmove, another listed property portal in the UK.

So, why such a difference in value?

This is something I constantly tell entrepreneurs. Many times, business owners look at multiples from other transactions or listed companies and expect buyers to pay the same for their company. But the reality is that size and market leadership make a huge difference in valuation. In this case, Idealista was valued at almost 2.5 times Fotocasa’s EBITDA multiple, and frankly, it is not unreasonable: the leader generates almost 10 times Fotocasa’s EBITDA and 5 times its revenue.

I usually tell my clients that a strategic buyer often pays more than a private equity fund. But in this case, the opposite happened: the one paying high multiples was private equity (Cinven), and the one paying adjusted multiples was the strategic buyer (Scout24).

The German company is publicly traded with multiples of around 11.8x revenue and 26.7x EBITDA. However, it bought Fotocasa and Habitaclia at 2.6x revenue and 14x EBITDA. That is, it paid more than 75% below its own revenue multiple and around 45% below its own EBITDA multiple.

For a listed company, it makes sense to pay less than the price at which it trades: if it pays more than what the market values its own shares at, investors usually penalize the stock price. What is striking here is the very large “discount” relative to its own valuation.

Cinven, on the other hand, has no such limitation. A private equity fund thinks in terms of medium-term exit value (usually 4–6 years). They calculate what the company could be worth within that horizon, under certain assumptions of organic growth, geographic expansion, or acquisitions, and apply a reasonable exit multiple. From there, they discount back to determine the maximum price they can pay today and still achieve the return they seek (usually with leverage included).

In other words, while a listed company like Scout24 is constrained by the short-term market, a private equity fund like Cinven focuses on expected IRR and its future business plan. This explains why it can pay higher multiples if it believes it can grow, expand, and sell at a higher price in a few years.

Time will tell. What is certain is that Idealista, being considerably smaller than its German peer (1/3 of EBITDA), was valued at an EBITDA multiple even higher than Scout24’s:

Is this valuation sustainable? We’ll have to see.

Cinven only entered a year ago, and if it follows a typical five-year plan (common in private equity), it needs substantial growth to justify that value. In Spain and Portugal, organic growth potential is limited, so perhaps the key lies in expanding to new markets and acquiring portals (or software) at low multiples, like Fotocasa and Habitaclia, then integrating and revaluing them within the Idealista ecosystem. That multiple arbitrage could turn an apparently expensive deal into a profitable investment for the private equity fund.

And here I return to something I often say: selling to a strategic buyer (or competitor) usually allows for higher valuations than selling to private equity. But obviously, this is not always the case. For a strategic buyer to pay a high multiple, there must be clear synergies with the seller, and perhaps in the case of Fotocasa/Habitaclia, there weren’t: Scout24 was entering a new country in its real estate business and may not have seen substantial synergies to justify paying more.

On the other hand, I am aware that I am comparing apples and oranges: a private equity fund entering a large market-leading company versus a strategic buyer acquiring a much smaller player. Yet, it is fascinating to see how much multiples can vary in relatively mature business models, and how size, growth, and leadership remain the biggest drivers of value in M&A.

By Joshua Novick, partner at Bondo Advisors

Source: https://joshuanovick.substack.com/p/por-que-idealista-vale-20-veces-mas

cloud technology axon

Over little more than a decade, Regenera has built a strong track reco...