While the Stock Market Hesitates, the Private Market Keeps Buying

A Striking Coincidence

There’s an interesting coincidence. Just as we published the third annual edition of our M&A report on Software and SaaS 2025(you can download it here https://bondoadvisors.com/informes-bondo) , focused on valuations, buyers, and actual transactions, the market for publicly listed SaaS companies experienced a very sharp correction. In a single day, over $300 billion in market capitalization disappeared, and the IGV Software index had already fallen nearly 30% from its peak at the end of September.

This is by no means a negative signal. What this correction reflects is the market’s concern over the speed at which many software companies can adapt to the new environment dominated by AI, agents, and automation.

Paradoxically, many of the companies that have seen the largest valuation corrections are reporting record sales and historic profits.

The debate isn’t about current results—it’s about who will be able to reinvent their product and value proposition fast enough in a world that is changing at an unusually rapid pace.

The Public Market Hesitates, the Private Market Does Not

My bet, and that of many buyers who continue to acquire software aggressively, is that software companies start with an advantage. They have the customer base, industry knowledge, and data. Building AI- and agent-powered solutions on top of existing platforms is far easier than replacing them from scratch.

That’s why, even though the stock market hesitates, the private M&A market remains very active.

In fact, 2025 was a record year for software acquisitions in Spain and Portugal—the highest in the past five years. Buyers remain very enthusiastic, and many sellers are bringing their companies to market.

An Expanding TAM and an Uncomfortable Decision

The consensus is fairly clear. The TAM for software solutions is set to grow dramatically with AI, more devices, robotics, agents, and new industries. The question for a small company isn’t whether that growth will happen, but whether it is prepared to adapt. Incumbents have clear advantages, but they need to invest and evolve their products.

For many founders, joining a larger group with real synergies or having the financial backing of a Private Equity firm is not just a defensive move—it’s an opportunity to accelerate and play big in the coming years.

What’s Happening in Iberia

Some data from the report helps put this into context.

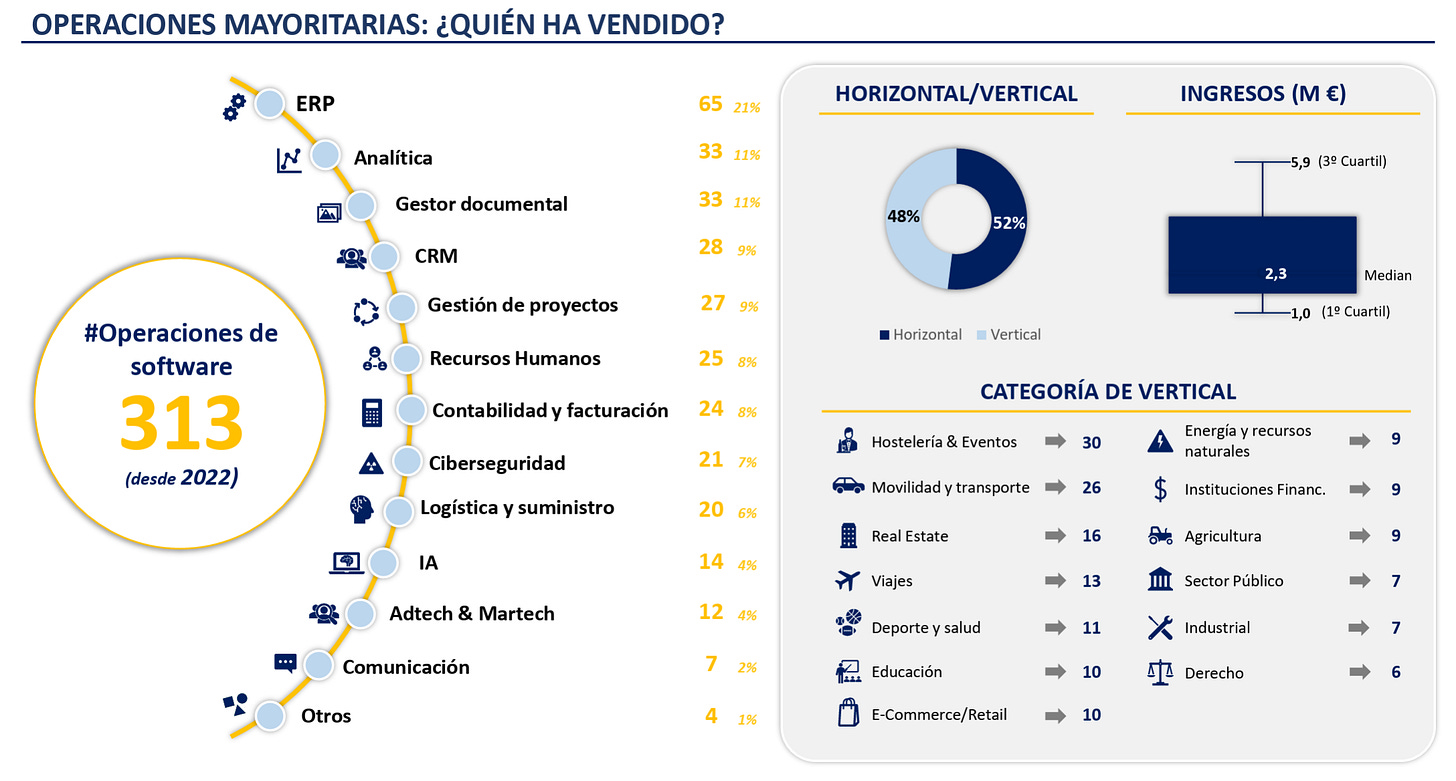

In 2025, 77 majority software deals were closed in Spain, compared to 66 in 2024 and 59 in 2023. This is the highest number of transactions in the past five years.

![]()

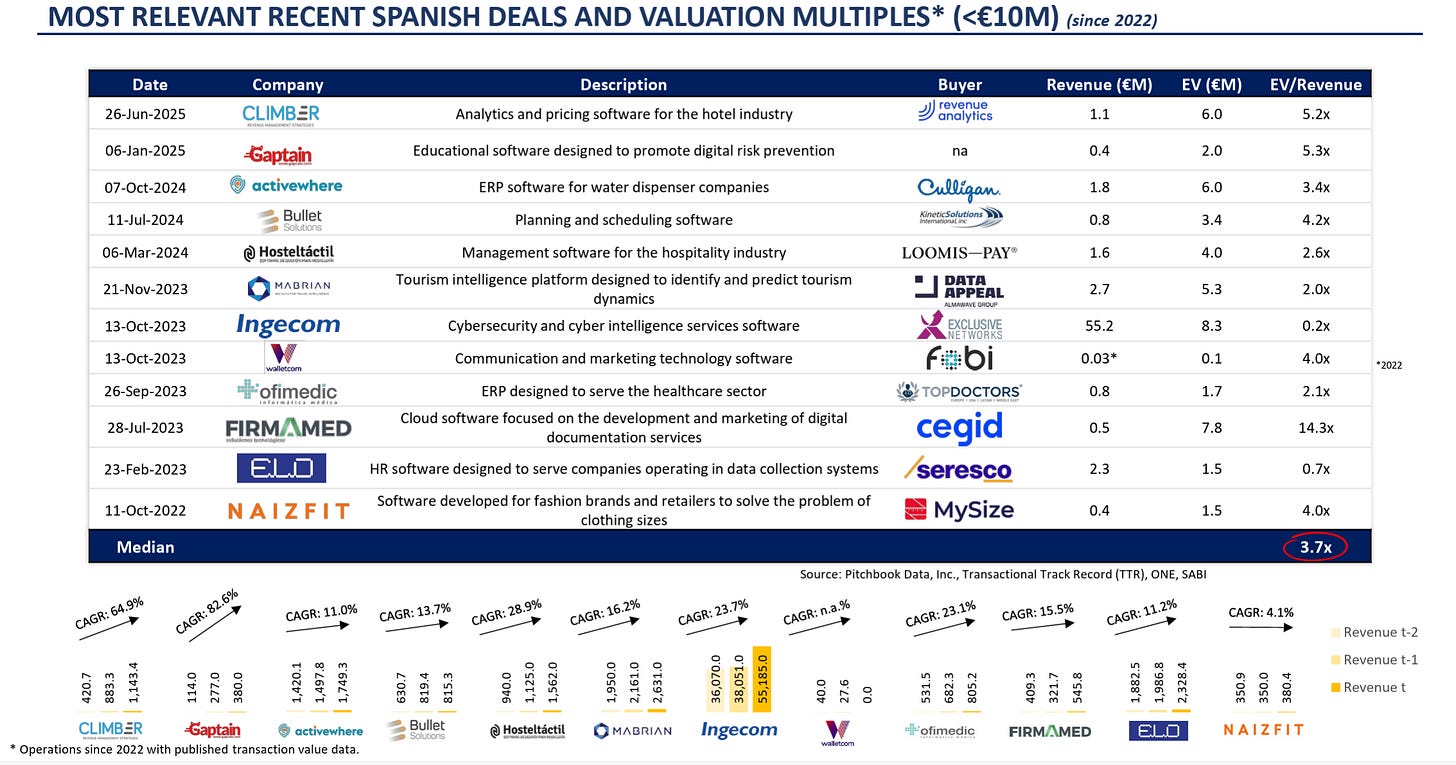

In smaller transactions, below €10 million in EV, the median valuation was 3.7x revenue.

In the range between €10 million and €100 million in EV, the median multiple rose to 4.6x revenue, reflecting a clear premium for size and quality.

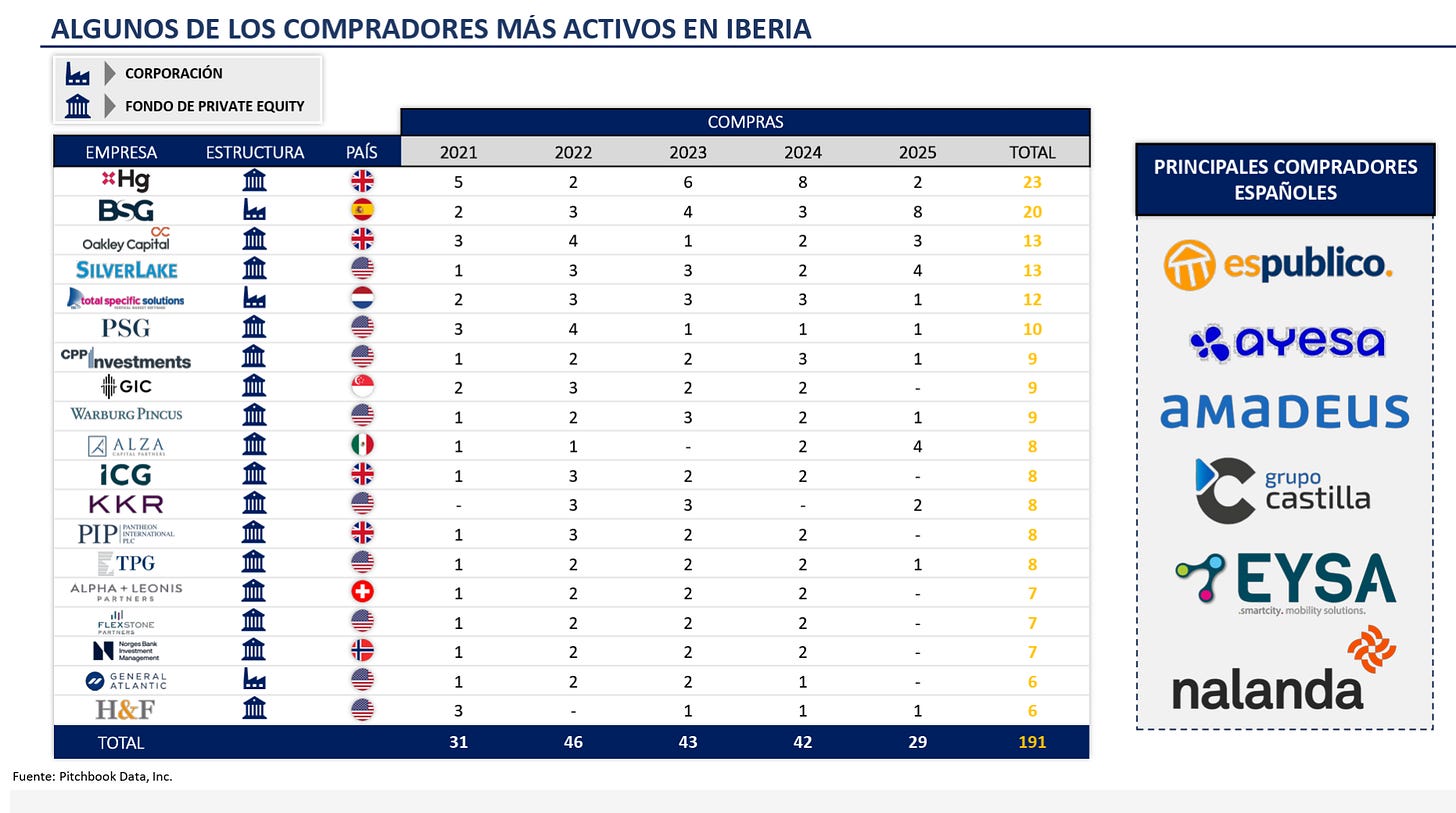

The most active buyers in Iberia over the past five years have clearly been Private Equity funds and software roll-ups. HG tops the ranking with 23 acquisitions, followed by BSG with 20. Next are Oakley Capital and Silver Lake, with 13 deals each, Total Specific Solutions with 12, and PSG with 10.

Rhe Full Report

The full report, with more than 30 pages of data and analysis, can be downloaded at

https://bondoadvisors.com/informes-bondo/

And if you want to discuss the current state of the software market or evaluate whether it makes sense to bring in a new majority partner or join a larger group, you can write to me directly at joshua@bondo.es

By Joshua Novick, partner at Bondo Advisors

cloud technology axon

Santander Corporate & Investment Banking has acted as Financial Adviso...