Market windows can't be predicted or controlled. They can only be seized—if you get there in time.

Between 1999 and early 2000, I raised $15 million for my startups. Just a few months later, I couldn't raise a single cent.

Nothing significant had changed in my businesses. Nothing unusual had happened. What had changed—dramatically—was the market. Investors' appetite for dot-com companies had vanished, and the window of opportunity had slammed shut.

Financial markets are defined by windows: windows of opportunity, open windows and closed windows. In a previous article, I wrote about the ideal moment to sell a company—just before it reaches its peak. Timing that moment perfectly is impossible, but entrepreneurs know their businesses better than anyone else. They have an instinct for where the company is heading and a certain degree of control over when to start a sale process.

Market windows are a different story altogether.

They have nothing to do with how well you run your business. You can't predict them. You only realise they're open once they're already open, and no one tells you when they're about to close.

What's more, every company has its own market window.

Some windows are macroeconomic. The 2008 financial crisis, for example, closed virtually every window around the world at the same time. Others are specific to a country. But more often than not, the relevant window belongs to a particular market. It might open for an industry—dot-coms back then, AI today—for a specific stock exchange, such as Euronext Paris during my IPO years, or for a sector going through a wave of consolidation, like web hosting during the acquisition frenzy I wrote about in a previous article.

Your window is the one that matters for your asset—not whatever happens to be making the macroeconomic headlines.

Wide open, half open, barely open and closed

Over the years I've developed my own taxonomy of market windows. You won't find it in any corporate finance textbook.

Wide open. The M&A market is in full consolidation mode, or investors are wildly enthusiastic about your type of asset, whether in venture capital or strategic acquisitions. Buyers compete against one another, valuation multiples expand, transactions move quickly, and even mediocre businesses find eager suitors. If you have a decent company to sell, buyers will almost take it out of your hands.

Half open. Deals are still getting done, but buyers have become selective. They're no longer buying the category—they're buying the individual asset. Multiples begin to compress, processes take longer, and due diligence becomes forensic. You can still sell, just not at the price you had in mind six months ago.

Barely open. There's still a faint breeze coming through the window, but only just. Only exceptional companies—or exceptionally cheap ones—get deals across the line. Most transactions drag on indefinitely or simply collapse before completion.

Closed. There's no money for anyone. Not even the best companies. Anyone who's lived through one of these periods knows this isn't a metaphor. The window hasn't just closed; it's been replaced by a brick wall.

The challenge is that the perfect exit requires two things to happen at exactly the same time: your company has to be approaching its peak, and the market window has to be wide open. The odds of those two conditions lining up are remarkably slim.

But when they do, you end up with the kind of exit people talk about for years—sometimes even to their grandchildren, who may still be enjoying the proceeds.

1999: When Anything with a Dot-Com Suffix Could Raise Money

I experienced my first market window from the inside, at the height of the dot-com bubble. Between 1999 and early 2000, I raised those $15 million for two startups: I-Network (which would later become Antevenio) and Demasiado.com.

It was a period of extraordinary euphoria. Even the most absurd business idea—and mine weren't—could raise money as long as it had a ".com" attached to it. The window wasn't just open; it had been ripped off its hinges. Capital was everywhere.

I raised money because the window was open, just like everyone else at the time. It slammed shut in April 2000 while I was in the middle of the roadshow for my next funding round.

I didn't manage to sell in time either, unlike several friends and peers who sold their companies for cash before the crash. Others accepted shares in publicly listed dot-com companies instead, only to discover that those shares were virtually worthless once the lock-up period expired. I'm talking about the people who got it right: Salvador Porte (LatinRed), Pep Vallés (Olé), Marcos Llamas and Marcos Enríquez (Ozú), the Elósegui brothers (Hispavista), and the Imaz brothers (MixMail), among other friends and colleagues who managed to achieve successful exits during those extraordinary years.

They sold while the window was still open. I was still in the middle of the process when it closed.

That's the nature of market windows. You can clearly see when they're open, but no one knows the exact moment they'll close.

Antevenio—the company I founded, took public and eventually sold in 2016—came dangerously close to running out of cash. Demasiado.com was sold to EresMas for pennies simply to avoid bankruptcy.

It was a challenging period—or, to put it less politely, a brutal one.

2007: The IPO Window That Lasted Only a Few Months

The next market window, in my own experience, came between 2005 and 2007, this time in the IPO market on Euronext Paris. That one, fortunately, we managed to seize.

We began Antevenio's IPO process in mid-2006 and listed in February 2007. Everything went remarkably well. The company was valued at four times revenue, at the upper end of our expected valuation range, and the offering was eight times oversubscribed.

A few months later, in the summer of 2007, the window began to close. Only a handful of particularly attractive companies were still able to go public. Then the global financial crisis hit in 2008, and everything stopped: IPOs, funding rounds, M&A—almost every type of transaction—for nearly five years.

This was no longer a sector-specific correction or a country-specific issue. It was a global recession.

The difference from 2000 was that this time I'd learned something.

I still had no idea when the window would close—nobody ever does—but after living through the dot-com crash, I knew it eventually would. That made speed my obsession throughout the IPO process. We tried to move as quickly and efficiently as possible through every stage of the listing.

Even then, we needed luck.

Any administrative delay could have cost us months. Spain's securities regulator, for example, had to delegate its authority to the French regulator, and that process could easily have dragged on. Had we started six months later—or had any stage taken longer than expected—Antevenio would almost certainly never have gone public.

When You See the Window, You Run—and Hope

Those two experiences taught me the only practical rule I'm willing to offer about market windows.

When the window is open, you go through it.

Even if your company hasn't quite reached its peak.

If your business is in good shape—it doesn't have to be perfect—an open market window is worth far more than the extra year of growth you think will increase your valuation.

The catch is that you never know whether you'll make it in time.

Whether you're raising capital, going public or selling a company, these processes take months, sometimes years. So you spot the open window, you start running, and you hope it doesn't close before you've signed the documents, collected the proceeds or, in the case of an IPO, rung the opening bell.

The only thing you truly control is execution: moving quickly, avoiding unnecessary delays and not wasting weeks at every stage of the process.

Everything else is crossing your fingers.

The Private Equity Windows

One of the best examples of how market windows open and close—outside the tech world—is private equity consolidation.

Right now, private equity firms are rapidly consolidating traditional industries that few investors paid attention to just a few years ago: fire protection and extinguisher inspection, elevator maintenance, swimming pool maintenance, accounting and payroll firms, and property management businesses.

If you own a company of reasonable scale in one of those sectors, chances are you have a queue of buyers knocking on your door.

These windows have their own dynamics, driven by the typical private equity investment cycle, which usually lasts around five years.

One fund starts consolidating a sector. Other funds adopt the same investment thesis, and before long there are five or ten platform companies acquiring businesses in the same market. They all begin at roughly the same time. Two or three years later, they all move into the next phase simultaneously: integrating what they've acquired, improving operations and preparing for their own exit.

Almost overnight, consolidation stops.

The window has closed, and the next wave of acquisitions in that sector may not come for another decade.

2026: In Tech, the Window Is Open Only for AI-Native Companies

Let's move to my own world, because technology is going through one of the fastest market-window shifts I can remember.

Today, the window is wide open for AI-native businesses, both in venture capital fundraising and in M&A.

According to data compiled by Windsor Drake, AI-native software companies are trading at 25–30x revenue, an enormous premium over traditional software businesses.

Meanwhile, in the space of just a few months, raising capital has become extraordinarily difficult for almost any startup that isn't AI-native.

Try raising a venture capital round today for a traditional SaaS company, a marketplace, an e-commerce platform, an edtech, a fintech or an insurtech business. It's not impossible, but only founders with exceptional track records and companies with outstanding traction are getting funded.

Software M&A tells a similar story.

The window hasn't completely closed, but it has gone from wide open to half open in the space of a single quarter.

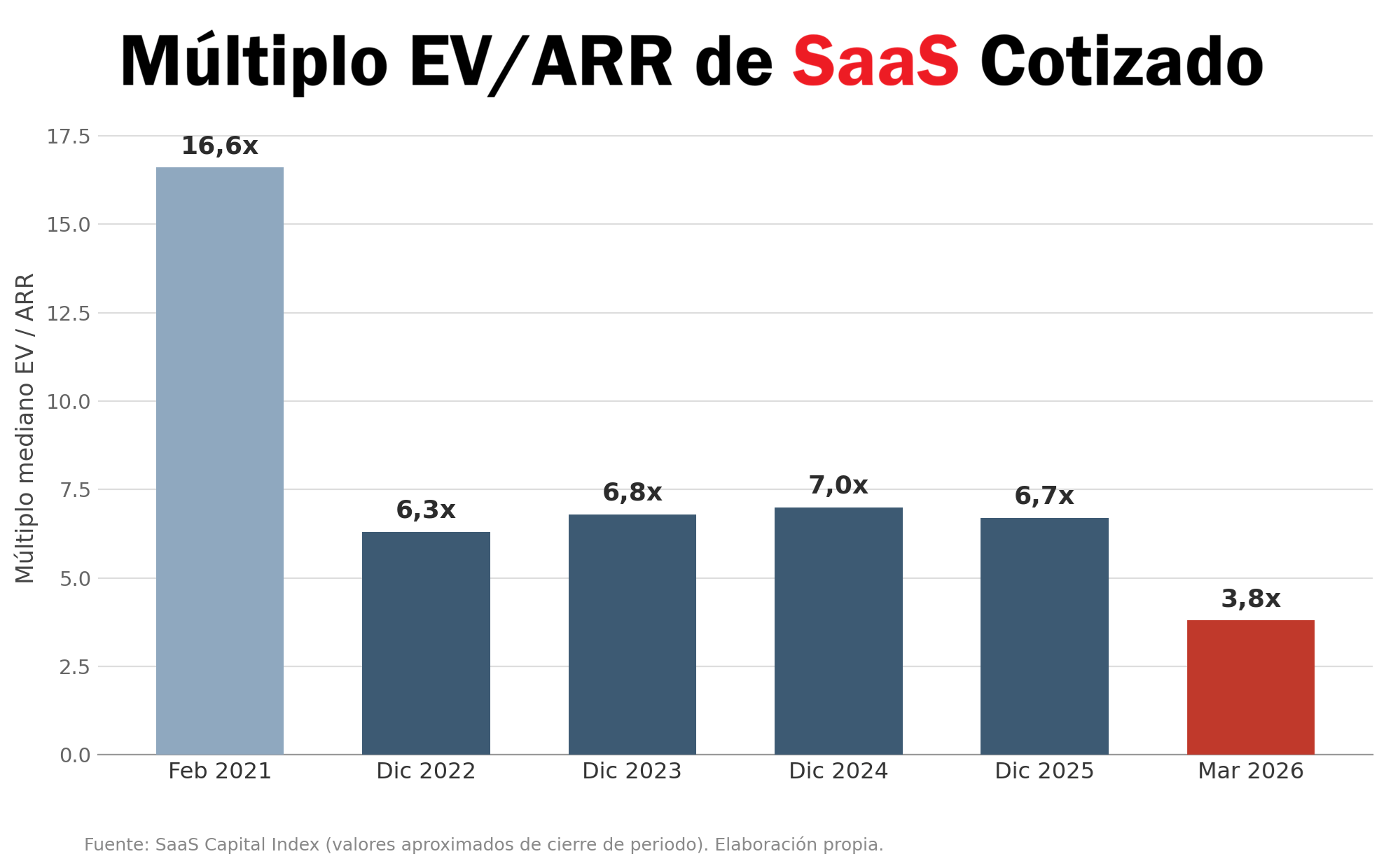

Public markets usually signal these shifts first. The median valuation multiple in the SaaS Capital Index fell from around 6.7x ARR, where it had remained for most of 2025, to 3.8x ARR by March 2026—the lowest level in more than a decade.

Salesforce is down more than 30% year-to-date. HubSpot has fallen almost 48%, despite reporting 23% revenue growth in the first quarter and beating analysts' expectations. Constellation Software—the world's most admired software consolidator—has lost more than half its value from its peak.

The market has even coined a name for it: the SaaSpocalypse.

This isn't fundamentally about business performance. It's about fear. Investors increasingly worry that AI will disrupt the traditional software business model, and they're discounting the entire category accordingly—good companies and mediocre ones alike.

In the private M&A market, where I spend most of my time, the impact arrives later—and with more nuance.

At Bondo Advisors, we still see active buyers for software companies. But they're asking tougher questions, negotiating harder, and no longer paying for the category itself. They're paying for the individual business: its churn, net retention rate, mission criticality, growth profile, Rule of 40 performance, and everything else that separates one software company from another.

A textbook case of a half-open window.

The Hardest Part Isn't the Closed Window. It's Your Mindset.

After living through several market windows, I've come to one conclusion: the hardest part isn't when the window closes.

It's adapting once it has closed—or when it moves from wide open to only half open.

When the window begins to shut, the market doesn't disappear.

What disappears is the price you had in your head.

Your valuation expectations are still anchored to six months ago, before the correction. The offer sitting on the table today feels almost insulting compared with the one you imagined back in December.

Meanwhile, the buyer is already operating in the new market.

That gap between the seller's expectations and market reality kills more transactions than any due diligence process ever will.

I saw it after the dot-com crash in 2001. I saw it again during the financial crisis in 2008. And I'm starting to see it now across technology businesses that aren't AI-native.

What do you do when you can no longer raise the capital you need to fund your burn rate or your next stage of growth?

What do you do when the valuation multiple buyers are offering today bears no resemblance to what people were talking about just six months ago?

There isn't an easy answer.

You either reset your expectations and make the most of the window that's still open, or you wait for the next one—knowing it may take five years to appear, as it did after 2008, or that it may never come at all.

Your company has to survive until then.

So that's what I've learned about market windows over the past twenty-five years.

I haven't managed to predict a single one.

Not one.

What I have learned is to recognise them when they're open, to move quickly when it's time to move, and not to argue with them once they've closed.

For now, that's enough for me.

Joshua Novick, Managing Partner at Bondo Advisors.

cloud technology axon

Santander Corporate & Investment Banking has acted as Financial Adviso...