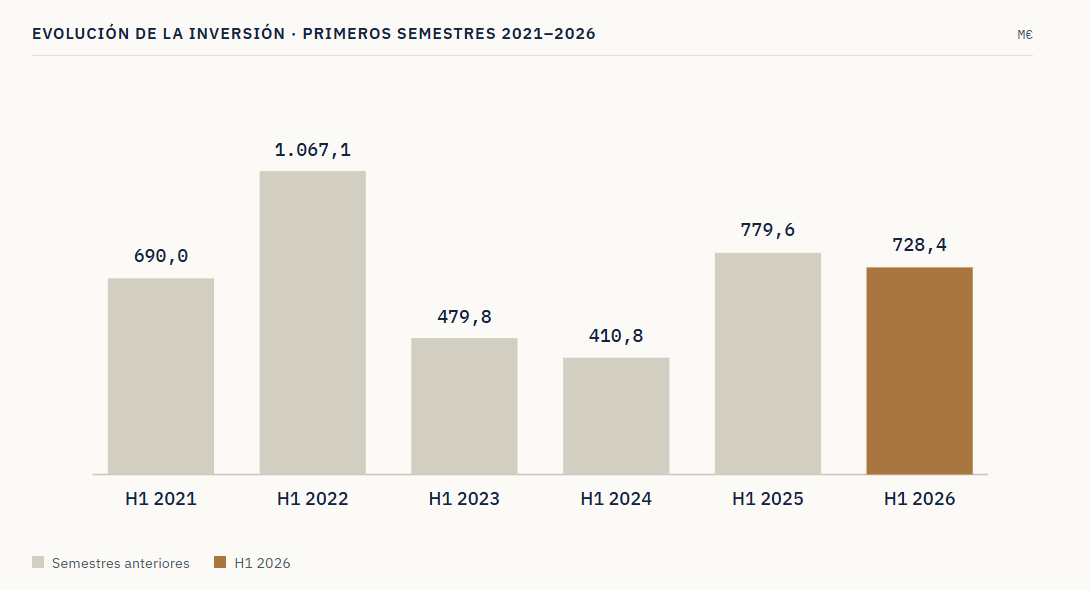

Venture Capital investment in startups founded or headquartered in the Region of Madrid reached €728.4 million during the first half of 2026, across 65 funding rounds, according to data from the Startup Radar madri+d platform on Dealroom. With this result, the first half of 2026 ranks as the third-highest six-month period on record by investment volume, behind only the first halves of 2022 (€1.067 billion) and 2025 (€779.6 million). The first half of 2025 had nearly doubled the investment recorded in the first half of 2024 (€410.8 million). These figures are consistent with the trend highlighted in the Startup Radar madri+d Annual Report (January 2026), available here.

Venture Capital investment in the Region of Madrid totalled €1.2 billion in 2025, representing a 97% increase compared with 2024. The average deal size reached €10 million (+122%), across 120 disclosed funding rounds (141 in total, including undisclosed rounds). This growth outpaced the overall European market, where Venture Capital investment increased by 59%.

Access the detailed semi-annual and annual investment figures.

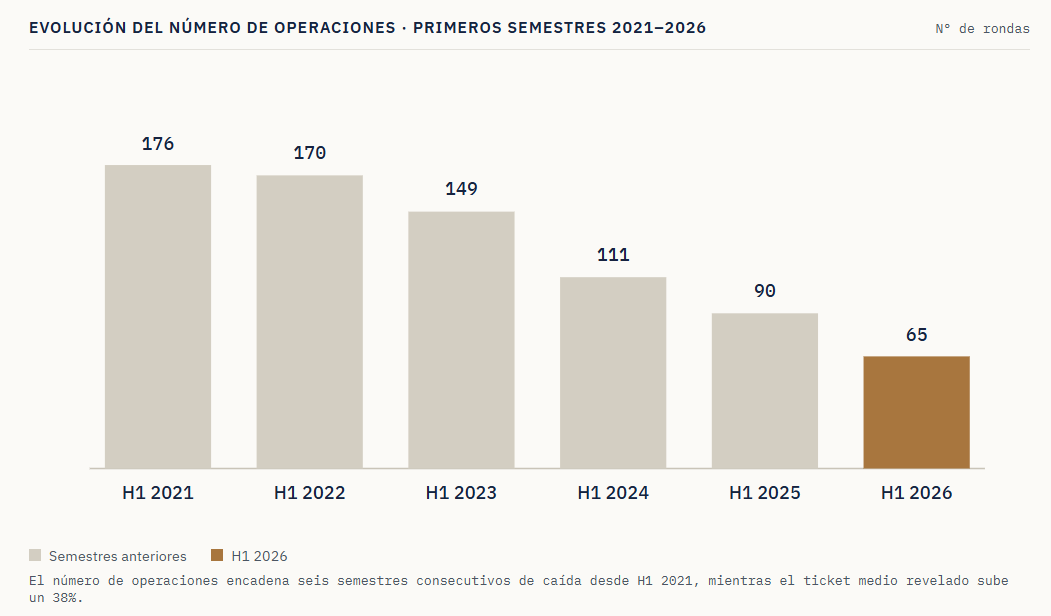

In terms of the number of funding rounds, the downward trend that began in 2021 continued. A total of 65 rounds were completed, compared with 90 in the first half of 2025, representing a 27.8% year-on-year decline and marking the fifth consecutive six-month period of decreasing deal activity. This decline was somewhat less pronounced than across Europe as a whole, where the annual decrease—also for the fifth consecutive six-month period—was 36%.

Access the detailed semi-annual and annual funding round

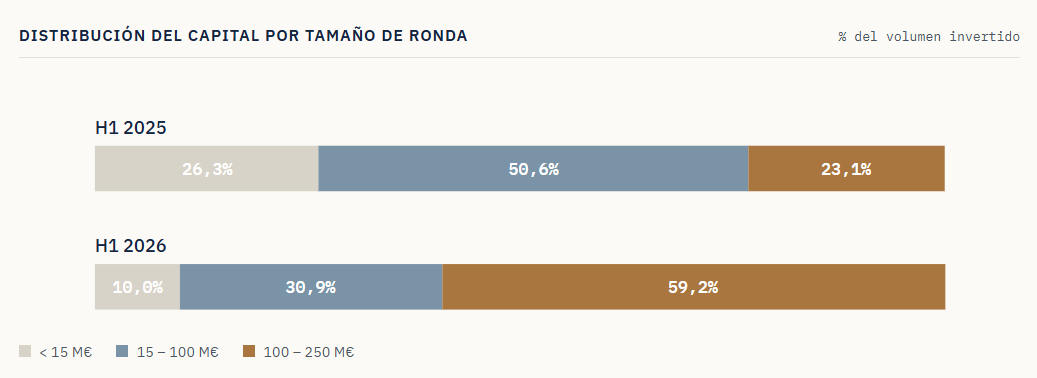

The result was a significantly higher average deal size—€14.0 million for rounds with a disclosed amount, compared with €10.1 million a year earlier—and confirms an increasing concentration of capital. Funding rounds above €15 million accounted for 90.0% of the total investment volume during the first half of the year, up from 73.7% in the first half of 2025. Within this segment, rounds between €100 million and €250 million alone raised €431.0 million, more than double the amount recorded in the same period of the previous year (€180 million).

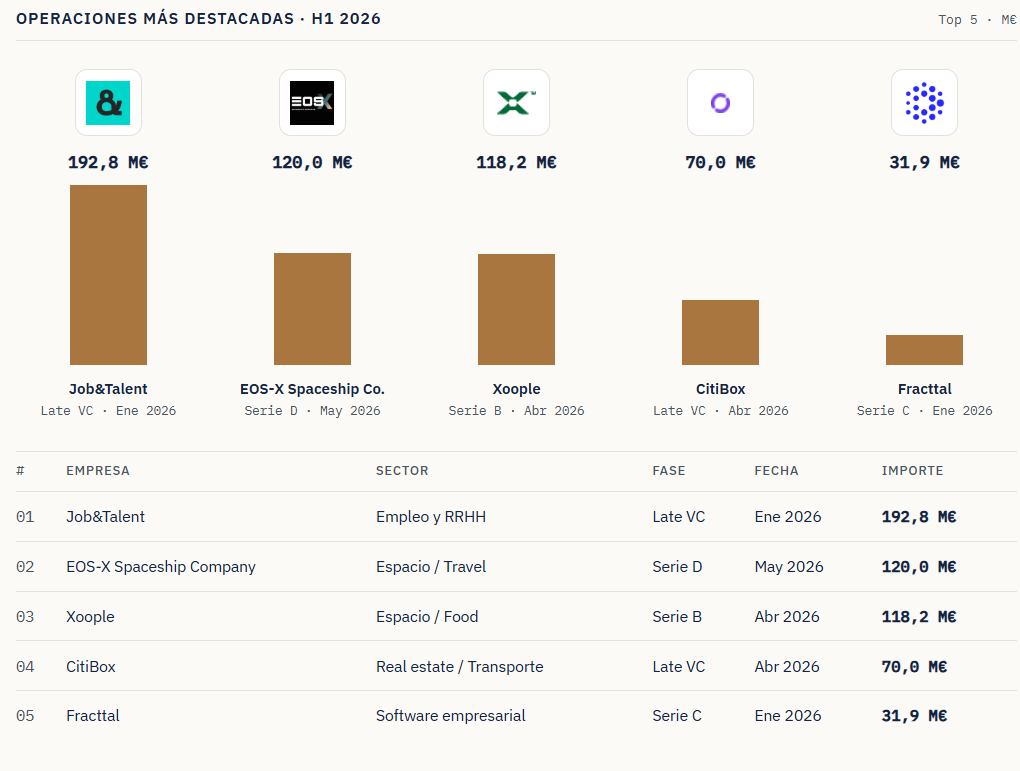

Job&Talent led the market with a €192.8 million funding round in January, followed by EOS-X Spaceship Company (€120 million, Series D, May) and Xoople (€118.2 million, Series B, April). The top five rounds were completed by CitiBox (€70 million, late-stage funding round, April) and Fracttal (€31.9 million, Series C, January).

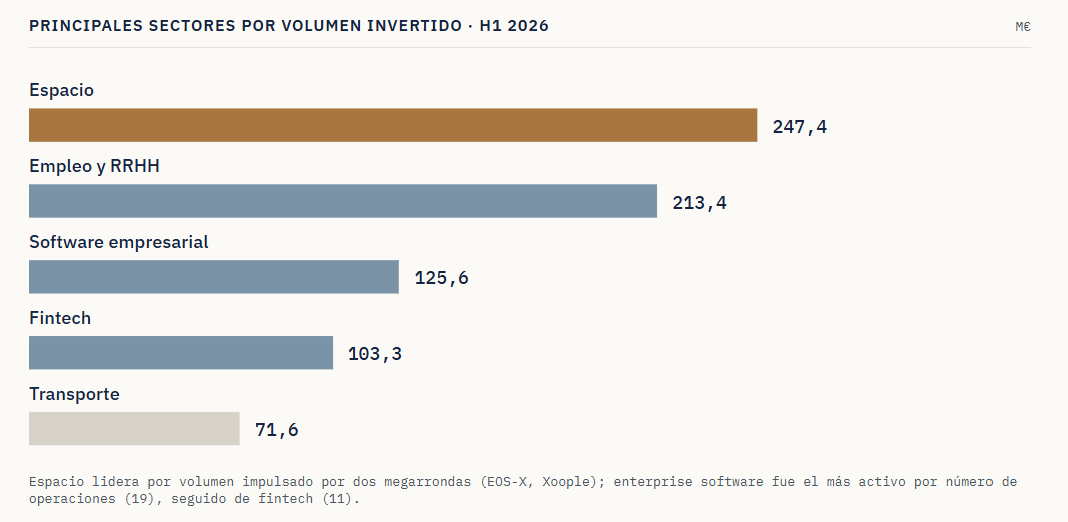

By sector, Space attracted the highest investment volume (€247.4 million), driven by the funding rounds of EOS-X Spaceship Company and Xoople. It was followed by Employment & HR (€213.4 million, largely concentrated in Job&Talent) and Enterprise Software (€125.6 million). Enterprise Software was, however, the most active sector by number of funding rounds, with 19 rounds, followed by Fintech, with 11 rounds raising a total of €103.3 million.

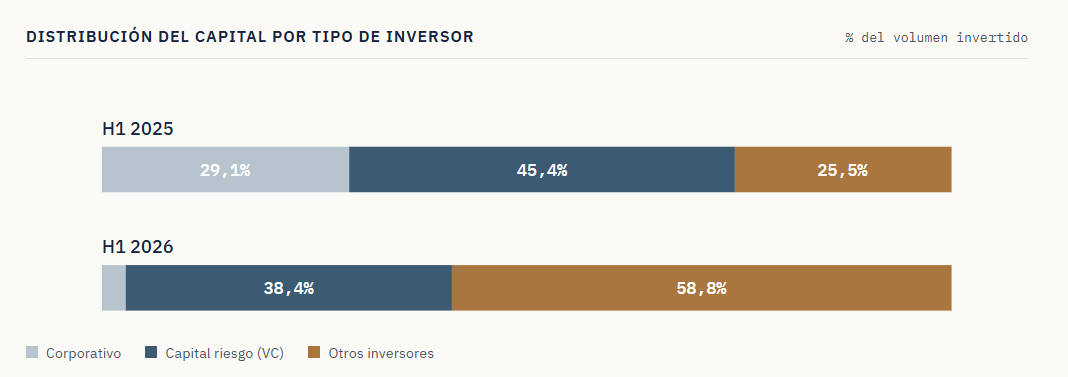

The breakdown by investor type shows a significant shift compared with the first half of 2025. Corporate investors sharply reduced their share of investment, from €226.6 million (29.1% of the total) to €20.6 million (2.8%). Meanwhile, the category that Dealroom classifies as "Other Investors"—those not categorized as traditional venture capital investors or corporate investors—accounted for 58.8% of total investment volume (€428.0 million), up from 25.5% a year earlier. Venture capital investors, in the strict sense, also declined in absolute terms, investing €279.8 million (38.4% of the total), compared with €354.2 million (45.4%) in the first half of 2025.

The distribution of investment by funding stage further confirms this pattern of concentration. Late-stage rounds raised €290.2 million across just five deals, accounting for 39.8% of total investment during the first half of the year. At the other end of the spectrum, seed-stage remained the most active segment by number of deals, with 29 funding rounds, but attracted a much more modest €34.4 million in total funding.

This contrast between a small number of large funding rounds and a much broader base of seed and early-stage deals with comparatively limited investment volume highlights the importance of early-stage access to capital. In this segment, the BAN madri+d Investor Network plays a key role in fostering investment by connecting private investors with technology-based startups through investment forums. The network does not invest directly in the companies; all investments are made exclusively by the private investors participating in the network.

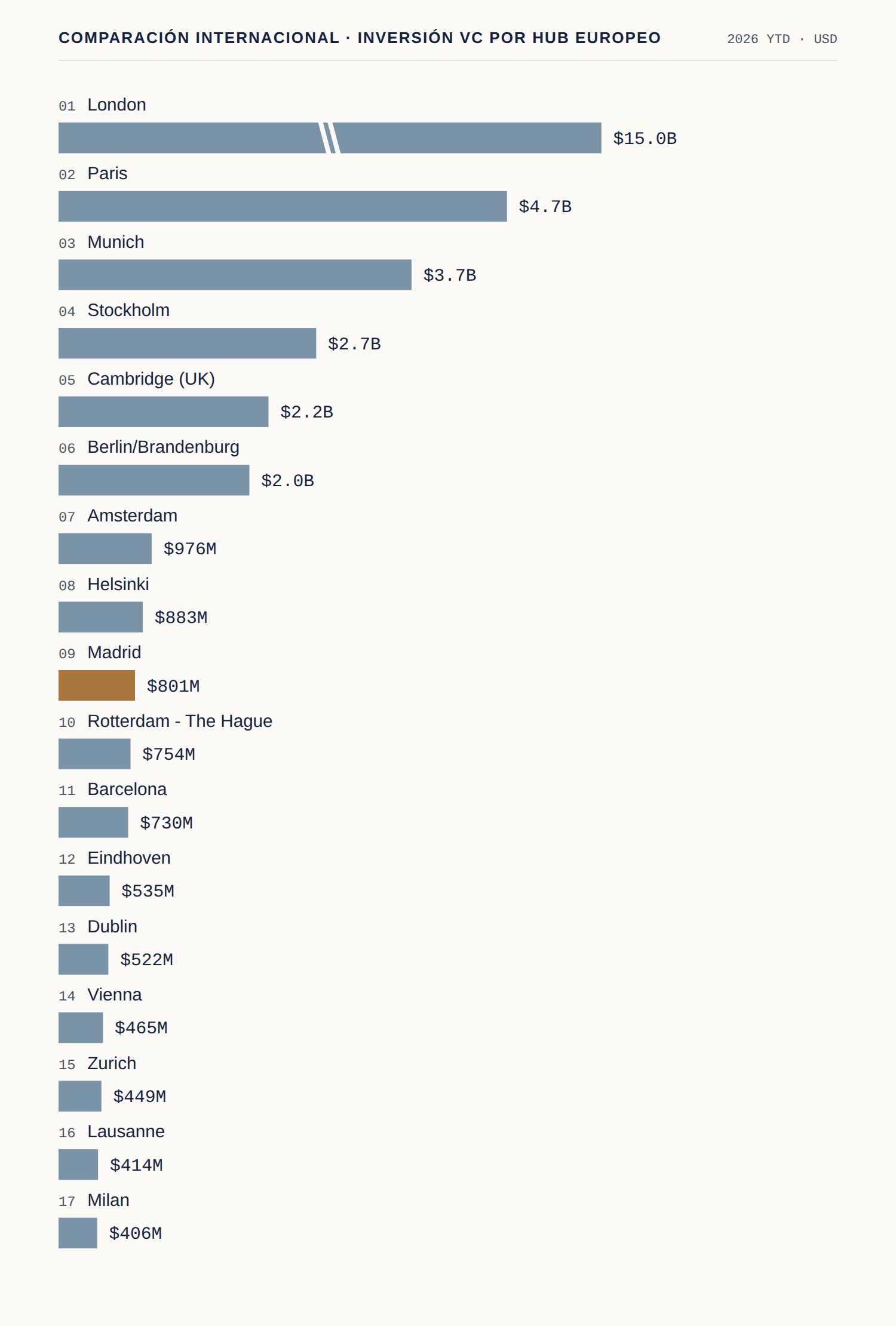

In the first half of 2026, the Region of Madrid ranked 12th among Europe's leading Venture Capital hubs by VC investment (YTD), with US$801 million invested.

View the full details at the link.

Although investment volumes remain below the historic highs reached in 2022, the trend in Venture Capital investment over recent half-year periods points to a strong and sustained recovery in the ecosystem. Against this backdrop, the BAN madri+d Investor Network remains committed to supporting the growth of startups and strengthening the investment ecosystem across the Region of Madrid.

The Business Angels Network (BAN) madri+d is a specialized investor network that helps innovative, technology-based startups in the Region of Madrid secure pre-seed and seed funding during their early stages of development. The network is promoted by the madri+d Foundation for Knowledge.

cloud technology axon

Santander Corporate & Investment Banking has acted as Financial Adviso...