Before moving forward with a sale process, the same fundamental question usually appears:

“Do I need both an M&A advisor and a lawyer?

Isn’t one of them enough?”

The short answer is yes, you need both.

But, as with most things in M&A, there are nuances.

To simplify, there are really two types of processes:

And depending on which situation you’re in, the combination “M&A advisor + legal advisor” may be essential—or not as much.

This is where many founders say:

“Since I already have a buyer, I’ll skip the M&A advisor and negotiate myself.”

It makes sense: theoretically, you save a 2% to 6% success fee—meaning hundreds of thousands of euros in fees.

But the reality is that many deals fall apart between the LOI and the closing, and this is precisely where the absence of an advisor tends to show its impact.

Even so, if you decide to skip the M&A advisor because you already have a buyer, there is something you cannot avoid:

You need a lawyer from minute one.

Among other things, for:

You need a lawyer specialized in M&A, with real transaction experience and who knows exactly what they’re doing. Not just any lawyer with corporate law experience will do.

Beyond reviewing contracts (usually drafted by the buyer) and the fine print, a good M&A lawyer is often a strong negotiator. In many cases, they can cover part of what an M&A advisor would normally handle—particularly when legal terms have direct economic implications.

In short: a generalist lawyer is not enough.

You need someone who understands deal dynamics and M&A market practices.

Here, the M&A advisor is not just recommended: they are essential.

Not only for negotiating, but for something simpler and more critical:

A company can never put a “FOR SALE” sign on its door.

If the company starts calling potential buyers directly:

The result: uncertainty, stress, rumors, talent loss, and sometimes even revenue impact.

An M&A advisor prevents this by using:

Additionally, it’s almost impossible for a founder to identify all potential buyers on their own.

An M&A advisor:

This information is not on Google nor ChatGPT. It’s in paid databases (MergerMarket, PitchBook, TTR) and proprietary databases used by advisors.

Some sellers, trying to reduce initial expenses (when they already have an M&A advisor), bring in the lawyer only from due diligence onwards, and during SPA negotiation.

Not ideal, but it happens.

The recommendation is to have them from the beginning, even with a lighter role early on.

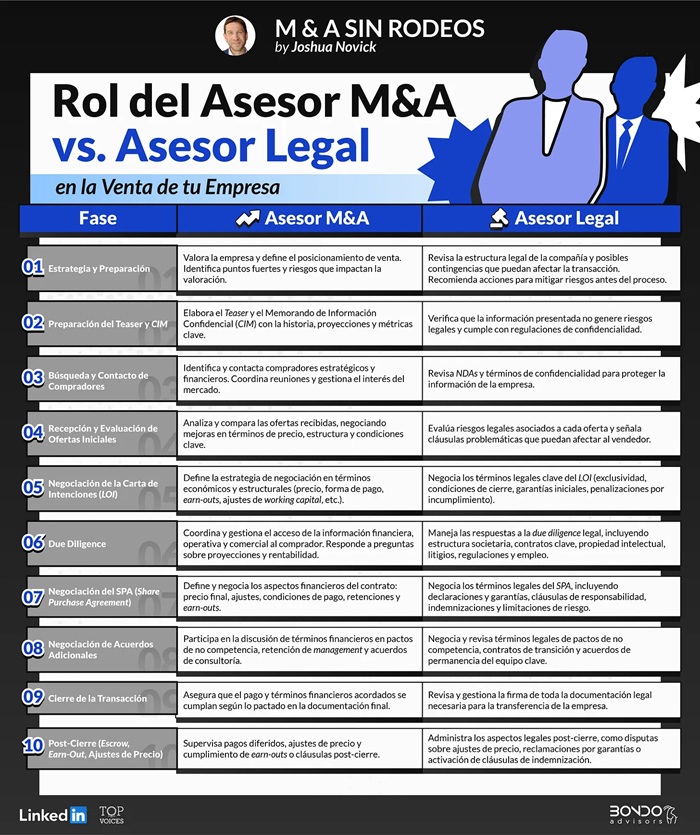

Below is the explanation of each phase, with additions and clarifications.

M&A Advisor:

Legal Advisor:

M&A Advisor:

Legal Advisor:

Usually not heavily involved, except when:

M&A Advisor:

Legal Advisor:

M&A Advisor:

Legal Advisor:

M&A Advisor:

Legal Advisor:

Some buyers use multi-page LOIs where they try to pre-negotiate key elements of the final agreement (price structure, exclusivity, indemnities, non-compete…).

In such cases, having a specialized M&A lawyer is essential, because a poorly drafted LOI can constrain you for the entire process.

And in some processes, the LOI is fully or partially binding.

When this happens, legal assistance from the beginning is not optional.

M&A Advisor:

Legal Advisor:

M&A Advisor:

Legal Advisor:

M&A Advisor:

Legal Advisor:

M&A Advisor:

Legal Advisor:

M&A Advisor:

Legal Advisor:

M&A Advisor:

Legal Advisor:

Something I often explain to founders, because almost no one mentions it:

It’s better if your M&A advisor and your lawyer are NOT from the same firm.

Why?

If both belong to the same firm:

This is why at Bondo Advisors:

No conflicts. No strange incentives. No interference.

Your lawyer protects you. Your M&A advisor maximizes price and gets the deal closed. Each one in their role.

By Joshua Novick, partner at Bondo Advisors

Source: https://www.joshuanovick.com/p/asesor-legal-vs-asesor-de-m-and-a

cloud technology axon

Axon Partners Group, Tresmares Capital, Sabadell Venture Capital, Inve...