Practical Guide to Maintaining Confidentiality and Attracting Buyers in a Company Sale Process

I’ve lost count of how many “blind profiles” I’ve received that, in reality, weren’t blind at all—they were an open book.

Sometimes the anonymity lasts a few hours, other times barely a few minutes. But in any case, what should be a confidential document often becomes, with a little curiosity and access to public sources, a fairly easy identification exercise.

Not long ago, I received a teaser that was supposedly “blind.” It didn’t mention the company name but included a very detailed description of what it did, the sector it operated in, its approximate location, the logos of its main clients, and the 2024 accounts with the exact figures of €2,898,962 in revenue and €765,872 in EBITDA (in this case, the numbers aren’t real so as not to give away clues).

With that information, within minutes, I could narrow it down to about five likely companies. I visited their websites, and one of them listed exactly the same clients. Out of curiosity, I went to the Companies Registry, typed in the SL’s name (which I found in the website’s terms and conditions), and bingo—the €2,898,962 in 2024 revenue was there.

It was still a teaser, but certainly no longer particularly “blind.”

In trying to make the document attractive and descriptive, many advisors or entrepreneurs end up giving away too many clues. Finding the balance between generating interest and maintaining confidentiality is not easy, speaking from experience. Give too much information, and anyone can identify the company. Give too little, and you risk scaring off potential buyers who don’t understand the company and its attributes.

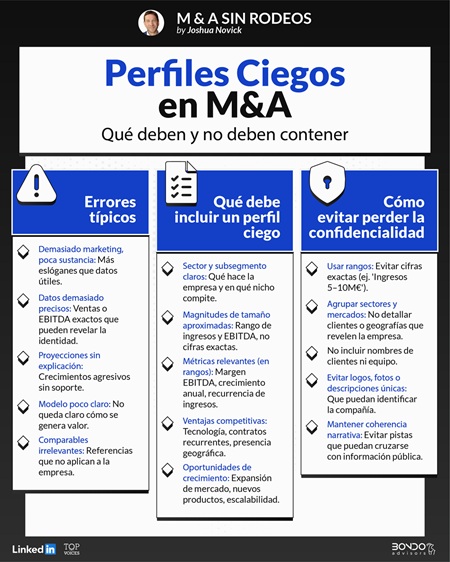

In the early stages of an M&A transaction, the blind profile, also called a teaser, is the first document a potential buyer sees. It’s like a business card—but without the name.

Its purpose is simple: generate enough interest so a potential buyer wants to know more and agrees to sign a non-disclosure agreement (NDA). Only after signing the NDA is the company name revealed, and the Information Memorandum with all the details provided.

The teaser isn’t just an “elevator pitch” without a logo. It’s a strategic document because how it’s written determines whether the buyer perceives the opportunity as worth their time and exploration.

A good teaser should provide enough information to capture the potential investor’s attention, allowing for a preliminary assessment of the opportunity, while not giving away so much that the company can be easily identified.

In practice, this translates into five main sections:

1. General Company Description

A very brief explanation of what the company does, the sector it operates in, and its business model.

Example: “Technology company specializing in SaaS solutions for the logistics sector, with clients in Spain and Italy.”

No exact locations or client names. If the company is in Valencia and the sector is small, simply stating “Spanish company” is sufficient.

It’s also common to include the approximate number of employees (e.g., around 25 when there are actually 23) and a generic reference to size (ARR of roughly €2M).

2. Strengths and Growth Opportunities

This section is meant to capture interest. Saying “innovative company in strong growth” isn’t enough; you need to highlight elements that make the opportunity attractive.

Examples:

The company’s strengths should be highlighted without exaggeration or hyperbole, e.g., “undisputed leader in its sector with revolutionary technology transforming the European market.”

3. Basic Financial Data

This is one of the trickiest points.

The goal is to give the buyer an idea of the opportunity’s scale while avoiding identification. Rounded numbers or ranges are recommended:

Example: “Revenue close to €3 million”

Never include exact figures or detailed balance sheet items, as they can be traced. You can also mention EBITDA margin (e.g., “operating margin around 25%”) or a growth reference (“average annual growth over 10%”).

4. Reason for Sale

Although brief, this is important for credibility. Buyers always want to know why the company is for sale.

No need for personal details. A strategic or financial reason is sufficient: “Seeking a partner to accelerate growth” or “Company without generational succession.”

5. Advisor Contact

Finally, the teaser should indicate who is managing the process and how to contact them—ideally with one or more emails and a mobile phone for quick calls or WhatsApp.

It’s standard to include the advisor’s name or firm, not the entrepreneur’s, which maintains confidentiality and channels inquiries professionally.

Equally important is what to avoid:

In short, anything that helps a buyer identify the company before signing the NDA should be omitted—unless it’s a core value of the business and excluding it would reduce interest.

A teaser serves four main purposes in an M&A process where buyers must be actively sought in an open, competitive process:

A poorly drafted teaser that doesn’t balance highlighting the company’s value with maintaining confidentiality can fail to generate interest or compromise the process.

Writing a blind profile is almost an art. Three objectives must be balanced: inform, attract, and protect.

If the document is too vague, the buyer won’t understand it and will disregard it. If too precise, a couple of searches will reveal the company.

A teaser should convey essence, not identity.

Experience is required—both to write it and to understand what information will pique the interest of the most likely buyer or investor.

Teasers are usually one to two pages, sometimes a single page, with summarized data, clear narrative, and professional, attractive design. The goal is that within two minutes, the buyer knows whether it’s worth signing the NDA.

Signing an NDA is a real effort: legal departments review it, assess risks, request changes, and senior staff spend time evaluating the opportunity. It’s a good filter to avoid casual curiosity, though some inevitably slip through.

Many entrepreneurs who sell without an advisor think they can manage this step themselves—making a list of potential buyers, sending emails, or calling them, sometimes even meeting in informal settings.

In practice, maintaining confidentiality this way is nearly impossible.

If enough doors are knocked on to make it meaningful (and not just contacting two companies), the likelihood that news of the sale leaks is very high. Once a client, supplier, or competitor suspects the company is for sale, the news spreads quickly, which can have serious consequences.

If a specific buyer is already identified, the process can be managed directly and carefully, ideally initially without writing, until the NDA is signed.

But for open market processes seeking multiple potential buyers—funds, industrial groups, or international investors—doing it without an advisor is a significant confidentiality risk and could jeopardize the deal.

A specialized advisor knows how to maintain confidentiality, draft an effective teaser, filter interested parties, avoid leaks, prepare and normalize accounts, build credible projections, prepare the info memo, manage contacts, negotiate, support due diligence, and more.

But what can I say—I am an advisor myself.

By Joshua Novick, Partner at Bondo Advisors

Source: https://www.joshuanovick.com/p/como-hacer-un-buen-perfil-ciego-en

cloud technology axon

Axon Partners Group, Tresmares Capital, Sabadell Venture Capital, Inve...