“How much is my company worth?”

The question everyone asks — and one that never has a simple answer.

The first thing any entrepreneur asks me when we discuss a possible sale is how much their company is worth. It’s perfectly normal. After years of effort and growth, you want to know whether all that work translates into a very concrete number.

On many occasions, I’ve responded with what I genuinely think:

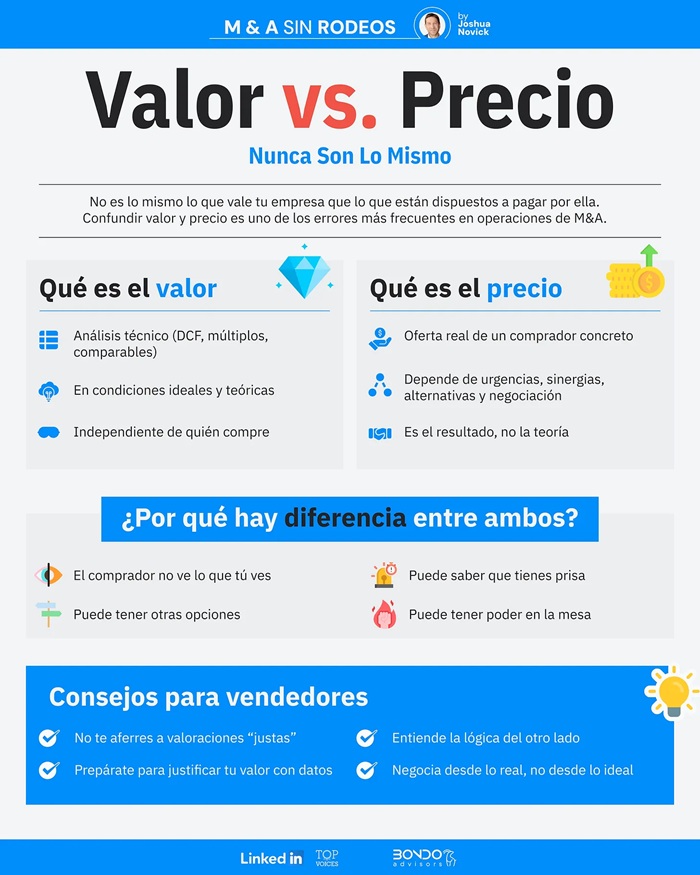

“Your company is worth what someone is willing to pay for it.”

Technically, that’s true — but let’s be honest: it solves absolutely nothing.

It’s a neat sentence and at the same time completely circular. And since no business owner likes it (for good reason), I stopped using it.

What can I do? I have to build valuations

The truth is that the value — or rather the price — of a company doesn’t exist in isolation. It isn’t a function of ARR, revenue, or EBITDA. Nor is it a number hidden in a spreadsheet waiting to be discovered. It depends on strategic fit, on where buyers stand at that moment, and on the environment you find yourself in when you go to market.

The difference between value and price is not a theoretical nuance — it is the essence of any M&A process.

You can have an excellent company and still not achieve a high price if the pieces that need to align simply don’t.

What needs to align for a high price

Companies sell at high prices when several factors come together, such as:

• there is a buyer for whom your company is a strategic fit

• that buyer is internally in a good moment to make acquisitions

• the financing environment makes deals easier to fund

• your company is showing strong revenue, growth and stability

Your company is only one of the factors — and not always the most decisive one.

Often, the price doesn’t depend on you, but on where the buyers are at that moment.

When the market isn’t aligned — even if you are

This situation is extremely common. You go to market with your SaaS business.

You’ve identified four logical buyers — two direct competitors and two large hardware groups for whom integrating your solution would make strategic sense. But you find that:

• one is in the middle of being sold to a new fund and can’t commit

• another has just changed its CEO and needs time before approving acquisitions

• another has just completed two large purchases and lacks internal capacity for a new deal

• another is focused on consolidating Northern Europe and won’t enter Spain until France and Italy are closed

Your company may be in an excellent moment — but if these buyers are not in a position to move, the price won’t reflect your best moment.

And this is where the difference between value and price becomes crystal clear.

Still, we always do a valuation

Even if the market will ultimately determine the final price, valuation offers a reference point. It is a theoretical estimate of the intrinsic value of the company, but it doesn’t incorporate the external factors that truly influence price — buyer timing, strategy, internal bandwidth and geographic priorities.

Despite its limitations, valuation is still necessary to understand a reasonable range.

And to build that range, we typically combine several methods.

How companies are usually valued in M&A

1. Public comps

Pros

• multiples updated daily

• good for observing trends

• transparent, complete data

Cons

• much larger and more stable companies

• geographies with different dynamics

• business lines not always comparable

• multiples not transferable to small companies

Useful to understand market sentiment — not to copy numbers.

2. Prior private transactions

Pros

• more comparable company sizes

• real prices paid by real buyers

• valuable if recent

Cons

• outdated data

• mix of fixed and earn-out components

• EBITDA ambiguous depending on each buyer’s definition

• invisible internal adjustments

• limited comparability due to margin, geography or model

Useful — but must be handled with caution.

3. Discounted Cash Flow (DCF)

DCF projects future cash flows and discounts them to today. It sounds elegant, but it depends entirely on projections.

In high-growth tech companies, those projections are often overly optimistic.

DCF works better for businesses with years of stable data on growth, churn, and retention.

Still, it’s important because the buyer will always perform their own DCF — using your projections as a base and adjusting WACC, terminal growth, etc. It’s a necessary exercise, though far from an absolute truth.

What you actually get by combining everything

You don’t get an exact number — you get a range.

A reasonable reference that helps avoid unrealistic expectations, but not the final price.

Generally, we don’t go to market with a price.

The number you name immediately becomes the maximum you’ll ever get.

And you can’t know how many bidders will show up or whether they’ll be in the right moment.

Many times we’ve gone to market with a reasonable expectation only to find that two buyers were exactly at the perfect moment to acquire that company. When that happens, the process turns into a real auction — and prices can rise well beyond what we would consider “market valuation.”

That’s another reason why naming a number early usually hurts more than helps.

Anchoring — why it rarely works

Anchoring is essentially the extreme version of naming a starting price:

you set a very high number to frame the negotiation at that level.

In theory it sounds useful.

In M&A, it almost always works poorly because it:

• reduces competitive tension

• signals a lack of realism

• turns your own number into your psychological minimum

There are rare cases where it makes sense — typically with financial investors (not strategic buyers) who have clear limits. In those situations, a reasonable anchor can work.

But these are exceptions.

In most processes, we prefer not to anchor.

By Joshua Novick, Partner at Bondo Advisors

Source: https://www.joshuanovick.com/p/los-metodos-de-valoracion-de-una

cloud technology axon

Axon Partners Group, Tresmares Capital, Sabadell Venture Capital, Inve...