Recent weeks have seen a renewed wave of scrutiny on private debt markets, driven by a combination of idiosyncratic credit events, liquidity dynamics in semi-liquid vehicles, and broader macroeconomic uncertainty. Headlines have increasingly questioned the resilience of the asset class in a context defined by persistent inflation, elevated interest rates, and rising geopolitical tensions.

However, a rigorous and technically grounded analysis suggests a more nuanced conclusion: while the cycle is clearly maturing and dispersion is increasing, the structural foundations of private debt remain intact. The current environment calls neither for complacency nor alarmism, but for disciplined optimism anchored in selectivity and risk management.

The purpose of this report is to separate short-term noise from the structural fundamentals of the asset class, offering a balanced view: reassuring in terms of systemic solvency, yet prudent regarding the risks that characterize the current phase of the market.

Recent headlines have focused on three main areas:

A technical analysis of each of these elements helps distinguish temporary noise from the industry’s structural foundations.

1. Idiosyncratic Situations: First Brands and Tricolor

First Brands and Tricolor have been presented as examples of structural vulnerability in private debt. However, a detailed analysis suggests that these are highly specific situations and not representative of core senior secured sponsor-backed direct lending.

First Brands was linked to complex structures with collateral over receivables, documentation controversies, and double pledging of assets. The identified risks are characteristic of asset-based financing with high operational complexity, not traditional corporate lending with robust financial covenants.

Tricolor featured a unique credit profile associated with subprime financing, granular collateral, and a dynamic different from middle-market sponsor-backed companies with stable EBITDA generation.

In both cases, the determining factors were specific to the business model and the particular structuring involved. Moreover, both cases included alleged irregularities that became subject to legal proceedings. They therefore do not appear to constitute evidence of generalized deterioration in underwriting standards in the core segment, but rather cases with highly specific structural and governance characteristics. Extrapolating these events to the entire asset class oversimplifies the technical reality.

2. Redemption Limits in Evergreen and Semi-Liquid Vehicles

3. Artificial Intelligence and Software Exposure

Market Indicators and Aggregate Data

Once the factors fueling media noise are contextualized, aggregate indicators of the private debt market show relative stability.

Yields have declined across all income-oriented assets, including private debt. However, according to the Cliffwater Direct Lending Index (CDLI), a widely used benchmark for U.S. direct lending, returns in 2025 were 9.33%, including expected unrealized losses from price markdowns of 54 bps. Spreads and SOFR have stabilized, leading Cliffwater to believe that current yields are sustainable.

Return generation continues to be supported by contractual carry, predominantly floating rate, which has captured elevated base rates during the recent cycle.

In addition, default rates are consistent with a mature phase of the cycle but remain far below from systemic crisis scenarios such as 2008–2009 or even the 2020 shock.

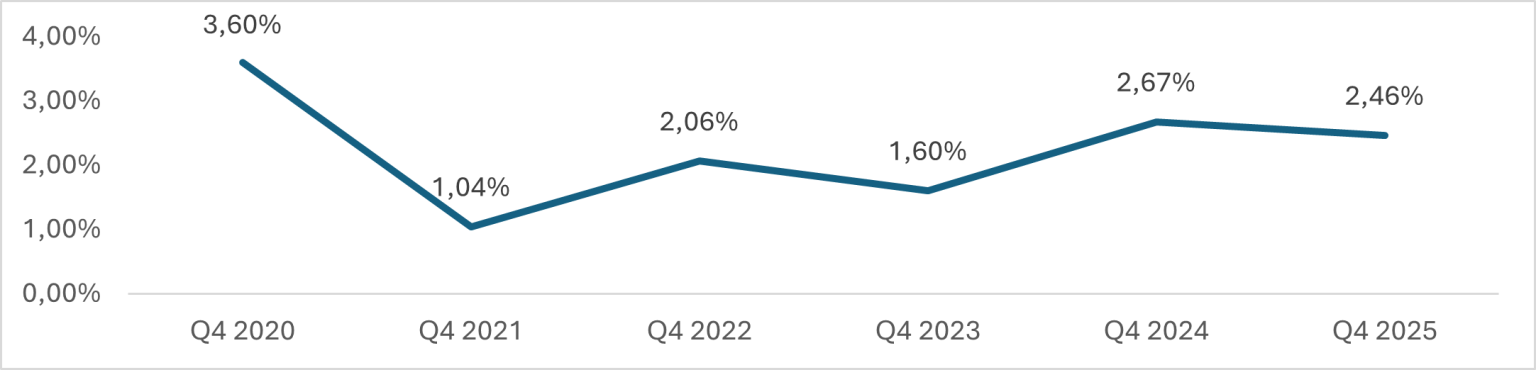

Proskauer Private Credit Default Index

Source: Proskauer’s Private Credit Default Index” As of January 26th, 2026

A good indicator that would contribute to prove credit quality and stability is that GP-led secondary transactions involving continuation vehicles are being executed at par or near par.

Illiquidity Premium and Market Segmentation

The illiquidity premium remains a key structural component. Although some spread compression1 has been observed in the upper mid-market (around 50–100 bps for higher-quality profiles), the lower mid-market continues to offer spreads 100–200 bps higher, in addition to OID and additional fees.

1. Source: Analysis by the AltamarCAM Private Credit team based on the overall market situation

This structural difference versus more competitive segments reflects reduced access to syndicated financing and greater operational intensity, maintaining attractive compensation for illiquidity. Structural seniority, the presence of real collateral, and direct negotiation capacity with sponsors also provide stronger downside protection mechanisms than liquid syndicated markets.

Manager Dispersion and AltamarCAM Positioning

2. Source: AltamarCAM. Includes the following private debt funds: Altamar Private Debt I, Altamar Private Debt III, Altamar Private Debt IV, and AltaCAM Global Credit II. Note: Past returns are not necessarily indicative of future results given that the current economic conditions are not comparable to prior conditions, which may not repeat in the future. There are no guarantees that the funds will have similar results as previous funds.

Current Risks

Despite structural elements that insulate fundamentals from media noise, a realistic approach requires acknowledging current market risks:

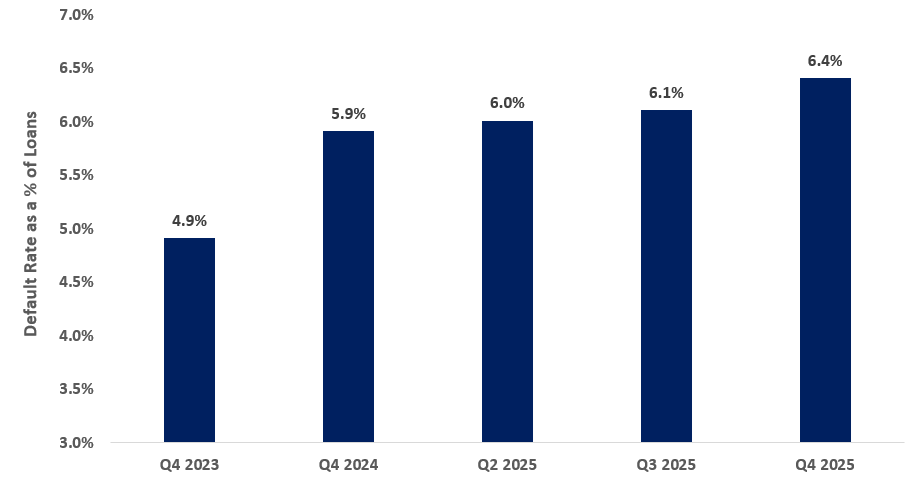

Private Credit ‘Bad PIK’ / Shadow Default Rate

Source: Lincoln International, Private Market Perspectives: U.S. Edition

We are not facing a systemic crisis, but rather an environment where dispersion will increase and asset class beta will be less decisive than selection alpha.

Distressed and Opportunistic Opportunities

This environment creates fertile ground for distressed and opportunistic strategies. The combination of widening spreads in special situations, the need for fresh capital in stressed structures, and the potential for secondary transactions in portfolios at discounts opens opportunities for managers with legal-operational analytical capabilities and mandate flexibility.

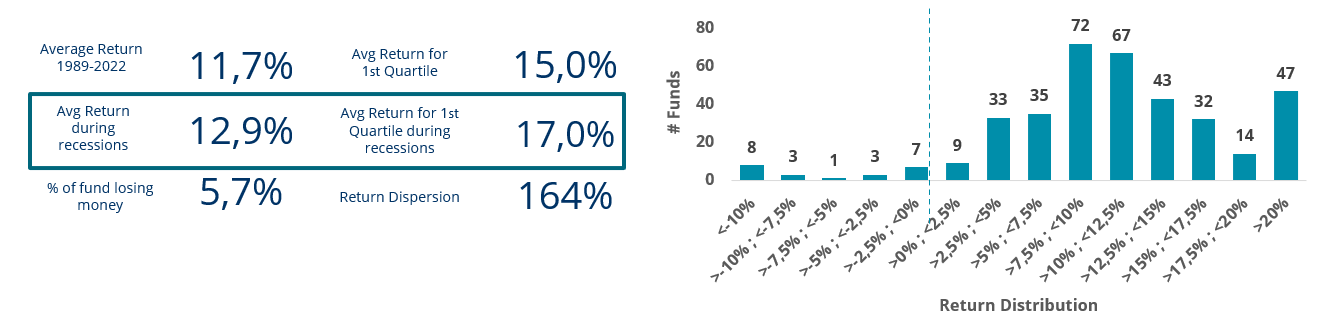

Opportunistic Credit Return Distribution

Source: Preqin and AltamarCAM Credit. Analysis done by Altamar using Preqin database. Total sample size of 388 funds. Sample size includes funds with a focus on North American and/or Europe with a size >$200Mn. Past returns are not necessarily indicative of future results given that the current economic conditions are not comparable to prior conditions, which may not repeat in the future. There are no guarantees that the funds will have similar results as previous funds.

Historically, distressed funds launched during phases of credit normalization have captured attractive returns through discounted acquisitions and active participation in restructuring processes.

Conclusion

cloud technology axon

This transaction reinforces Alantra’s continued momentum in Aerospac...