In an environment marked by structural currency volatility, managing exchange rate risk is key to preserving investment value. At AltamarCAM, our hedging approach seeks to protect returns while maintaining flexibility and cost efficiency—balancing discipline with adaptability across different market cycles.

The impact of currency movements varies significantly across asset classes. Long-term strategies such as Private Equity tend to naturally mitigate exchange rate effects over time, while shorter-duration or tighter-margin assets require more comprehensive hedging. Our goal is to align protection with the nature and expected return of each strategy, ensuring sustainable value creation for investors.

Preservation of investment value constitutes one of the fundamental pillars of AltamarCAM’ s investment policy. Among the external factors that may influence portfolio performance, currency risk stands out as one of the considerations that must be appropriately assessed and managed as it could affect the investments value. In this regard, long-term currency hedging strategies often entail significant costs and may not always prove fully efficient in achieving the desired objectives. Consequently, at AltamarCAM we implement a tactical and flexible currency management approach, tailored to the specific characteristics of each asset, with the aim of safeguarding returns and mitigating volatility.

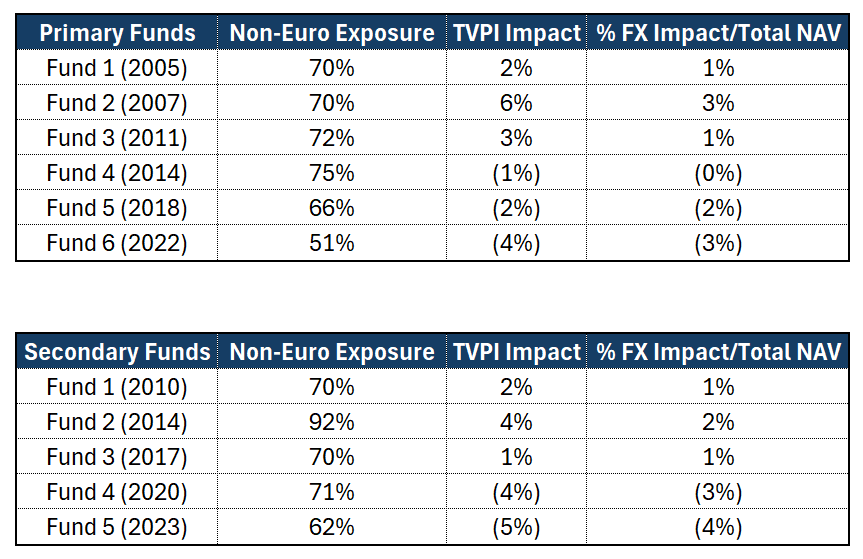

In the context of private market investments, where investment and divestment horizons are typically extended, currency risk tends to be mitigated over time as exchange rates normalize between entry and exit points, thereby reducing the overall impact of currency movements on portfolio valuations. Throughout our firm’s history, this mitigating effect inherent in long-term investment has been consistently observed across our portfolios. As an illustration, within the Private Equity segment—where certain funds maintain foreign currency exposures exceeding 60%—the overall impact on portfolio valuations has generally remained within a range of –3% to +3% (as of June 30, 2025, among the principal currencies to which we are exposed), resulting in a very limited effect on the final return to investors.

Currency Exposure and Its Impact on the Private Equity Portfolio

Hedging policy by asset class and strategy

Our currency hedging policy is designed to align with the expected return, investment horizon, and level of currency risk associated with each investment strategy. The following strategies are primarily employed, generally using forward contracts as the main hedging instrument:

Another important factor when determining the hedging strategy is the type of investment, particularly whether it is made through the primary market, secondary market, or co-investments.

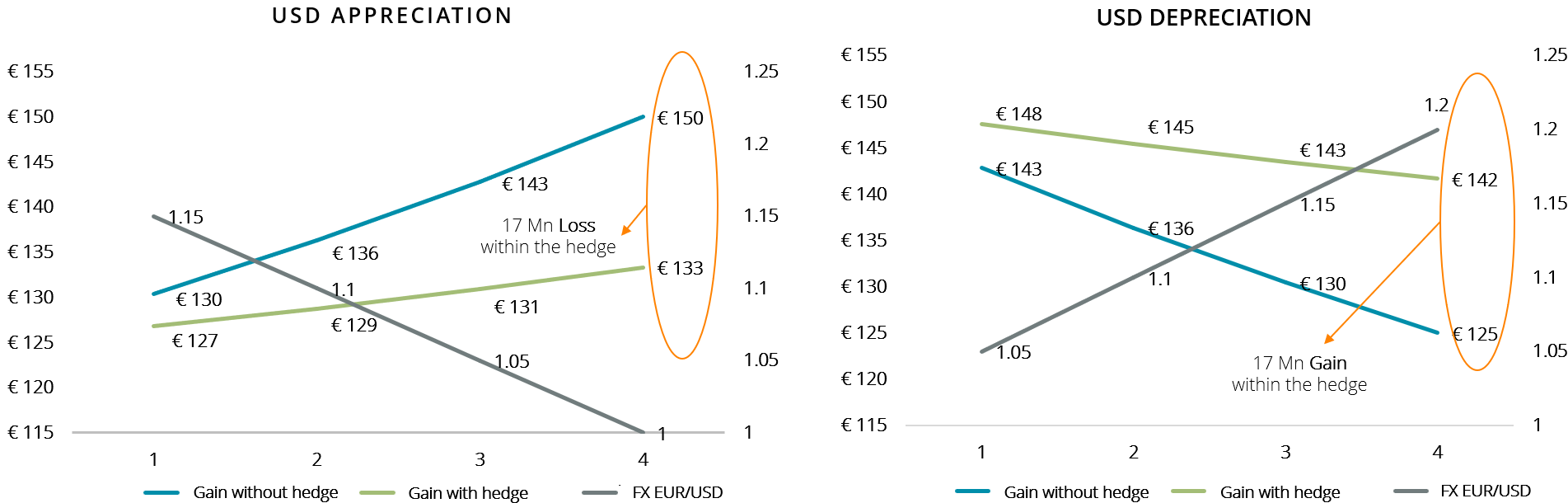

By way of illustration, the following section presents two scenarios demonstrating the effect of hedging in the event of both an appreciation and a depreciation of the U.S. dollar against the euro, using a base value of 100:

Market outlook

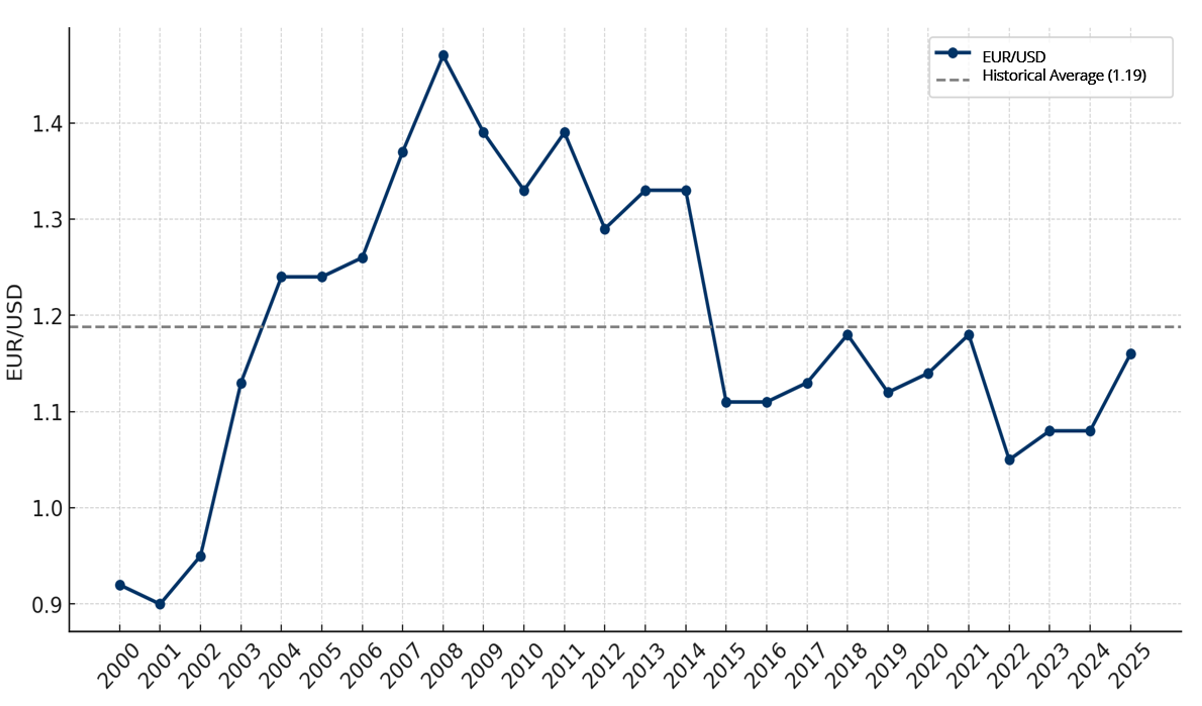

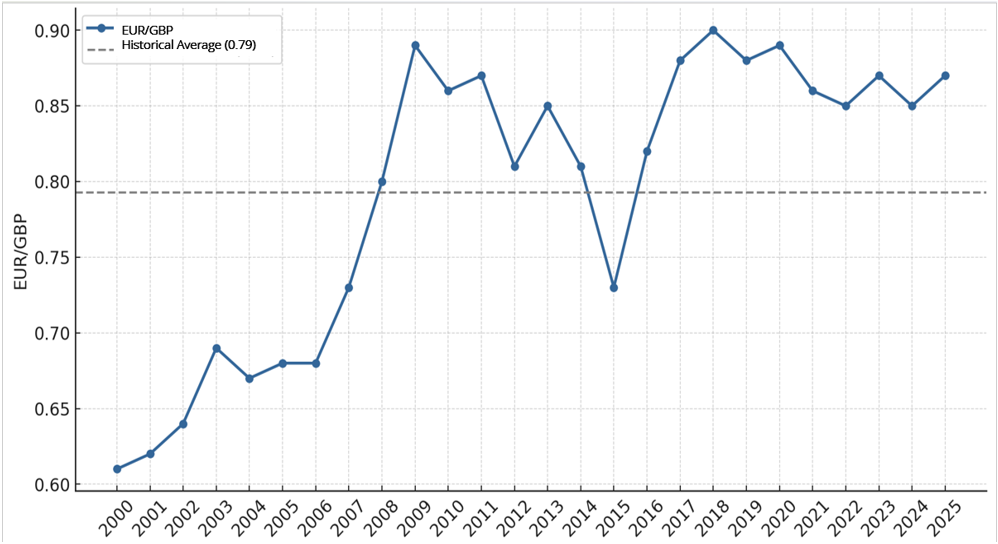

The performance of the U.S. dollar (USD) and the British pound (GBP) against the euro (EUR) over the past 25 years has exhibited high structural volatility, with the average exchange rates standing at approximately 1.19 for the USD/EUR and 0.79 for the GBP/EUR. This underscores the importance of maintaining a flexible hedging policy—one that balances discipline with adaptability to effectively navigate evolving currency dynamics.

Historical evolution of the Euro/USD (2000-2025)

Historical evolution of the Euro/GBP (2000-2025)

Future outlook

The short and medium-term evolution of major currencies will continue to be shaped by the monetary policies of the main central banks—notably the Federal Reserve and the European Central Bank—as well as by interest rate dynamics and the political environment in the United States and the United Kingdom. In this context, AltamarCAM’s strategy will remain focused on implementing tactical, selective, and asset-specific hedging, with the objective of preserving returns while avoiding excessive costs associated with long-term hedging instruments.

Conclusion

Currency hedging represents an additional tool for value preservation within alternative investment funds. AltamarCAM’s policy combines prudence, flexibility, and disciplined execution, trying to ensure that the management of currency risk does not compromise the return objectives of our investors.

cloud technology axon

This transaction reinforces Alantra’s continued momentum in Aerospac...