Car sharing’s origins date back to 1948 in Switzerland, with faster growth starting in the 1970s. The market has expanded further in the last two decades, driven by restrictions on city center private car use, advanced digital technologies, and shifting consumer attitudes around car ownership. However, it remains a relatively small market, accounting for less than 5% of the US $100 billion global shared mobility market.

Car-sharing schemes have faced a number of challenges, both for operators looking to build economically viable, scalable businesses as well as for authorities tasked with regulating them within and the overall mobility system. Looking ahead, car sharing has a key role to play in the integrated mobility system, in large part driven by increasing demand for sustainability and convenience. This Report explores the benefits and pitfalls of car sharing and describes strategies for success for both regulators and operators.

Car sharing has the potential to come into its own as a critical part of future mobility systems, alongside fixed route public transport (buses, trains, metros), on-demand public transport (ride hailing, ride sharing), micromobility (bikes and scooters), and deliveries and services (logistics, couriers). Indeed, a properly framed car-sharing scheme offers three main benefits. First, it improves the overall performance of the mobility system by enhancing connectivity, increasing access, and increasing system capacity. Second, it contributes to better sustainability and safety by significantly reducing the number of privately owned cars. Third, it offers the convenience of a private vehicle for users picking up goods, trip chaining,[1] or traveling out of town.

However, when car sharing is not properly framed into the overall mobility system, there are some pitfalls. For example, free-floating schemes (those without fixed parking stations) may encourage users to choose cars over mass-transport modes. There may also be cleanliness/condition issues from improperly maintained vehicles and some stationary vehicle nuisance issues (although less so than bikes and scooters).

Cities and transport authorities have struggled to regulate car sharing for two main reasons. First, regulation has often been overly restrictive, focused on limiting the scheme’s impact, rather than collaborating with operators to maximize overall mobility system benefits. In some cases (e.g., Car2Go in Toronto), limitations on area access and parking led to operators exiting the market altogether. Second, inadequate coordination between authorities across jurisdictional boundaries has often led to inconsistencies that confuse users.

The key challenge for operators is the business model. Many struggled to achieve profitability due to high operating costs, poor coordination with competitors, narrow focus (e.g., premium niches or B2B customers requiring costly customization), unfavorable revenue-sharing models with municipalities, and/or lack of collaboration with vehicle OEMs. Finally, inadequate parking arrangements with authorities have depressed customer uptake, as have delays in essential upgrades for operators relying entirely on third parties for their digital platforms.

Success in this market requires evolving car-sharing schemes beyond the traditional and OEM-led models. Future schemes must integrate better with the broader shared-mobility system and place services in locations where they add the most value.

We refer to this as the “ecosystem player stage.” Key features include designing the system around simplifying mobility for the user, using car sharing as a complement to the public transport backbone in both city centers and outskirts (including possibly providing subsidies for trips that are less profitable but benefit the overall system), and designing the system to suit as many consumers as possible (low/middle rather than premium).

For city authorities, this translates into seven imperatives:

For operators, we identify five imperatives:

As the shift away from car ownership continues and new mobility models become better integrated into the overall mobility system, car sharing has the potential to deliver major benefits to both customers and transport authorities. Looking further ahead, as autonomous vehicles (AVs) and robotaxis become more mainstream, we can expect car sharing to converge with ride sharing.

Car sharing is a component of the mobility offering in many major cities today, with a global market of about $3 billion and a predicted forecast of 20% CAGR over the next decade. More than 250 operators provide services in around 3,000 cities, about 30% of the world’s total. It’s nevertheless a relatively small part of the approximately $100 billion overall shared mobility market: less than 5% of the total.

The first recorded implementation of a car-sharing scheme was in Zürich in 1948 (known as the Selbstfahrergenossenschaft scheme). Further development of cooperative schemes took place in the 1970s and 1980s, mainly in Switzerland and Germany, although also in other countries on a smaller scale. Growth has accelerated in the last two decades, driven by rising traffic congestion, restrictions on private cars in city centers, digital technologies like mobile apps, and a gradual shift away from a desire for individual car ownership, especially among younger adults.

As post-pandemic pressure to develop and improve urban mobility systems continues, car sharing has a vital role to play, both in reducing private car journeys and as a complement to public transport systems. However, integrating car sharing within the mobility system has proven challenging for cities and transport authorities.

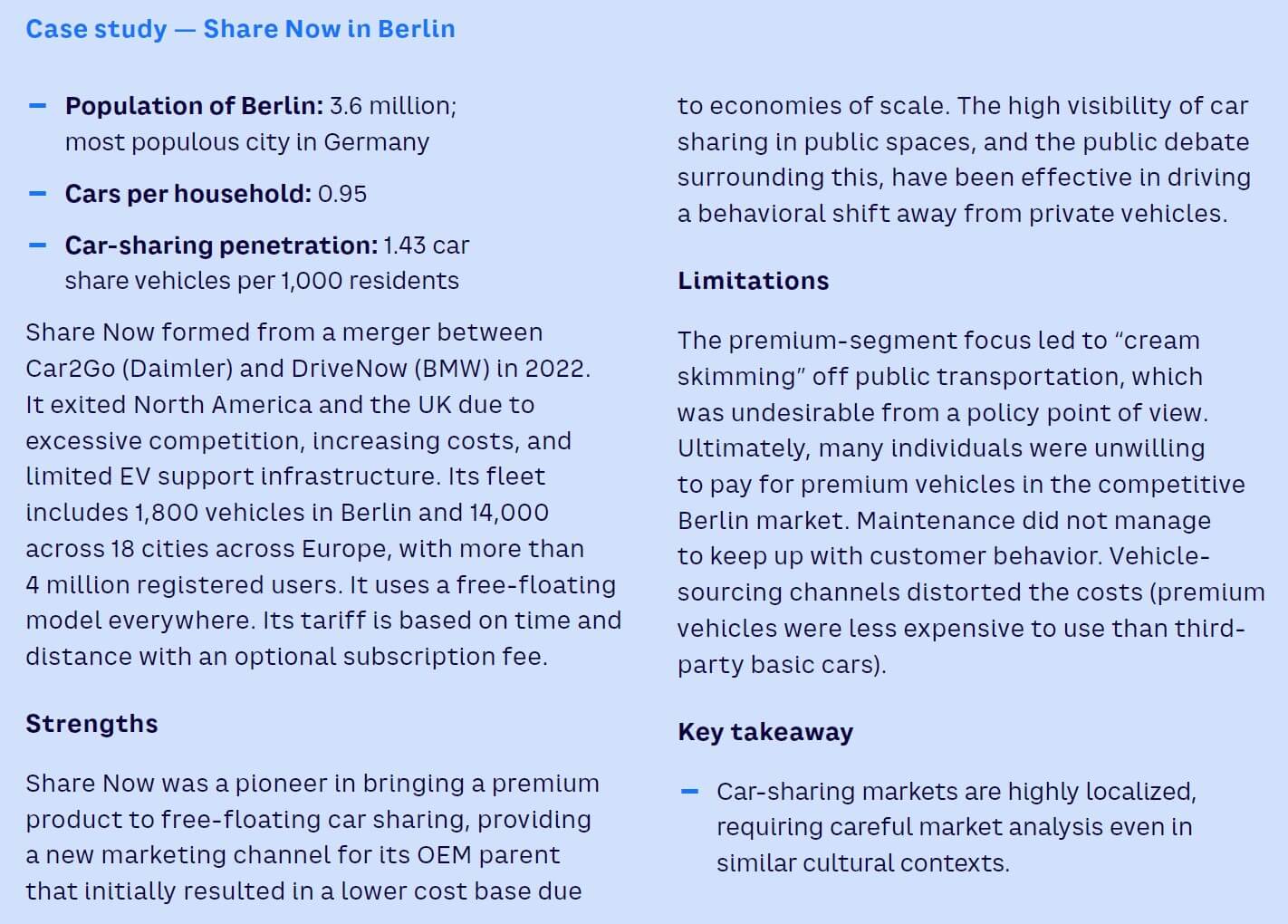

From an operator’s perspective, car sharing has not been without its hurdles. Although analysts expect double-digit market growth per annum in the coming years (driven by increased consumer willingness to use shared modes and a regulatory push to steer people away from private cars), the financial business case for traditional (i.e., asset-heavy) car sharing is uncertain. Many new ventures struggled for profitability, including Share Now, a 2019 joint venture between Daimler and BMW that combined their car-sharing services (Car2Go and DriveNow, respectively). Following the formation of the joint venture, Share Now pulled out of North American and British markets. Three years later, after losing €123 million in 2020 and €70 million in 2021, Daimler and BMW pulled out altogether, selling the business to Stellantis, operator of Free2move.

This Report explores the drivers, benefits, pitfalls, and strategies for success for car sharing, drawing on lessons learned from across the world. We draw conclusions for both transport authorities and operators on how, using the right ecosystem-based approach, car sharing can achieve its full potential as an essential part of the mobility system.

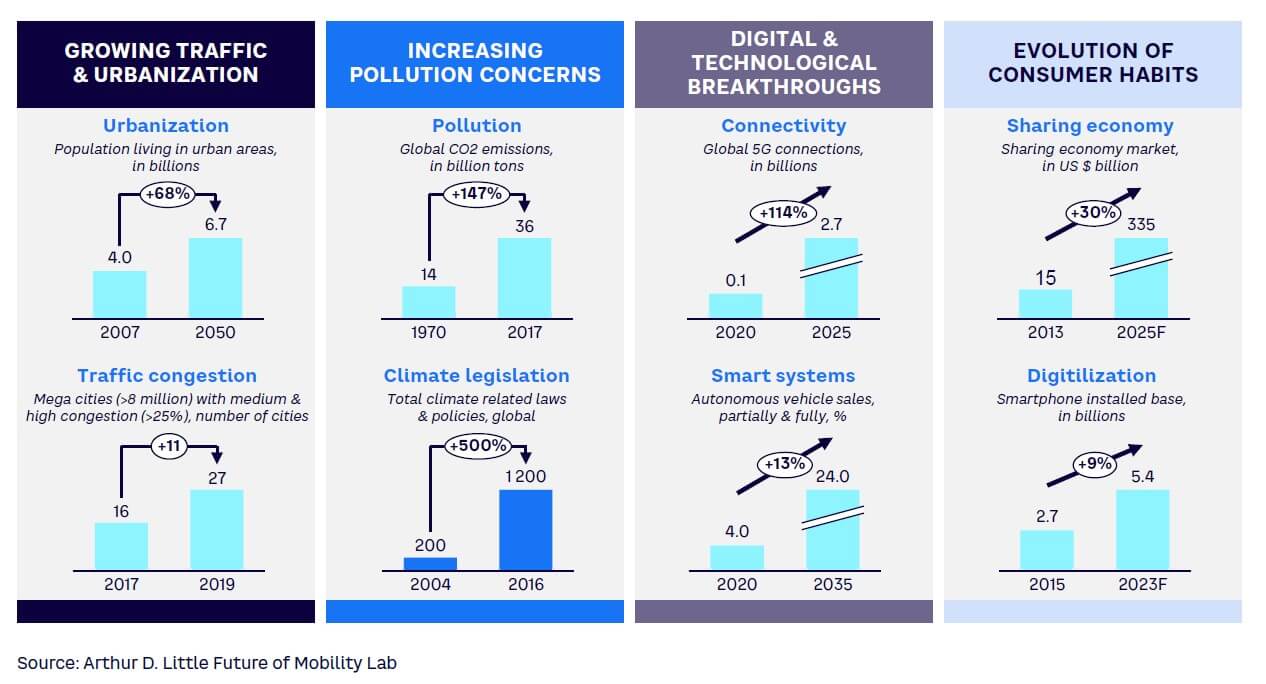

Several trends are shifting users away from private car ownership toward use-based mobility models such as car sharing; these are likely to increase over the coming years (see Figure 1).

We see from Figure 1 that urbanization is expected to increase significantly in the next few decades, bringing with it increased traffic congestion in the absence of improved urban mobility strategies and policies. Environmental pollution therefore has become an existential threat, causing many users to shift to EVs or avoid car ownership altogether. Digitalization will continue to change the way we interact as human beings, both socially and in a business context. Although we can envisage increased use of virtual and augmented reality for leisure, social, and commercial activities, it is unclear to what extent virtualization will affect mobility demand in the long term. What’s clear is that increased connectivity and usability of digital technology acts as a strong driver toward participating in the sharing economy, including shared mobility solutions.

We can predict with some confidence that the range and flexibility of mobility offers will grow in the coming years, with increasing degrees of convergence between them. Leasing rates are likely to rise, converging with car-rental and car-subscription models as short-term leases become more available. Car subscription, in which a car is provided for a month or several months with all costs and services included except fuel, is a rapidly growing model. Traditional car rentals (less than a month) will continue, but some of this market share will start to move to car subscription and car sharing. Car sharing and car subscription are increasingly converging into “car-as-a-service” (CaaS) offerings that center on flexibility and choice in terms of contract type and duration, vehicle model, and vehicle availability.

Although they have encountered more barriers and difficulties than envisaged five to 10 years ago, as illustrated by the 2023 Cruise-based robotaxi deployment in San Francisco and Dubai, AVs will also impact the future of car sharing. They will be deployed initially in urban areas as robotaxis or on specific routes, such as to and from airports, but will eventually accelerate a mindset shift away from car ownership by stimulating demand for car-sharing models, including nonautonomous conventional vehicles.

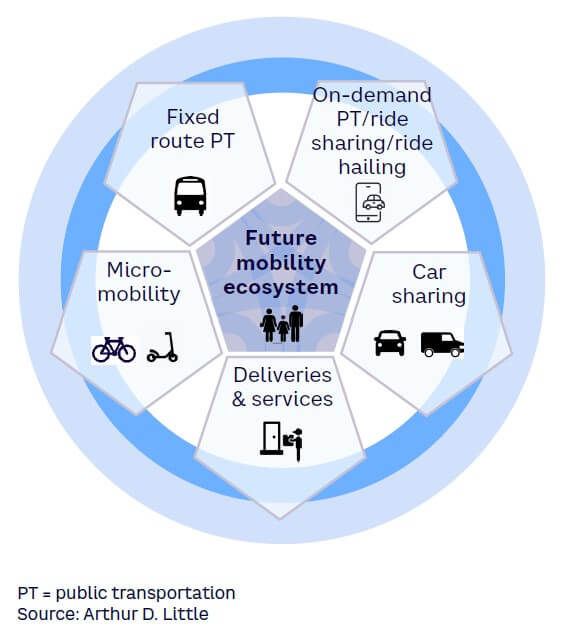

Car sharing is part of the future mobility system, alongside fixed route public transport, on-demand public transport, small vehicle sharing (bikes), and deliveries and services (see Figure 2). Potential benefits of car sharing fall into three categories:

Properly regulated, operated, and integrated with the wider mobility system, car sharing has the potential to deliver a range of performance benefits to cities and transportation authorities:

Car sharing provides several safety and environmental benefits:

Notwithstanding the significant potential benefits, if car sharing is not properly framed and integrated into the overall mobility system, it can have unintended consequences that detract from overall system performance. These include:

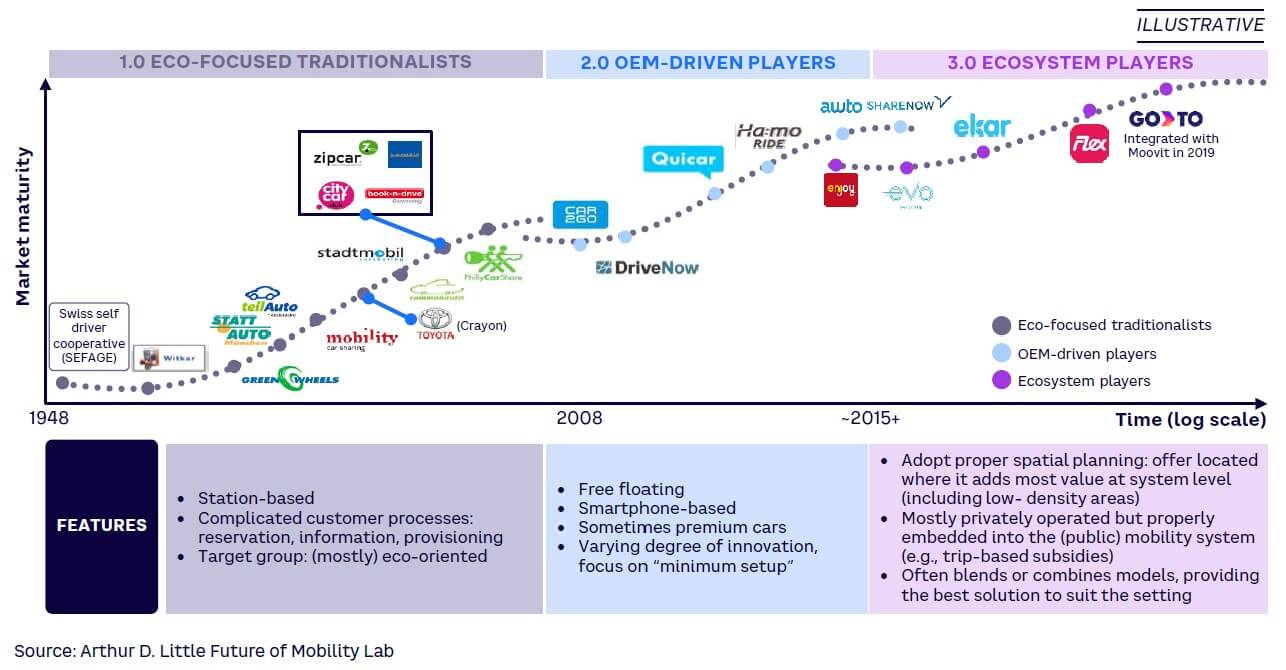

In 2014, Arthur D. Little (ADL) and the International Association of Public Transport (UITP) published “The Future of Urban Mobility 2.0” study, which described three stages of evolution: eco-focused traditionalists, OEM-driven players, and a third stage in which car sharing became a mass-market offering within an integrated mobility system.[5] Today, we can now be more certain and specific about the third stage, which we now refer to as “ecosystem players” (see Figure 4). There are existing operators in all three stages:

The next two sections look closely at the limitations of current models and explore how ecosystem players can overcome them.

The struggles cities and transport authorities face in regulating car sharing fall into two main categories: (1) overly restrictive regulation and (2) lack of coordination across jurisdictional boundaries.

Regulators sometimes view car sharing as a for-profit industry that provides additional mobility mode for users but is not a fully integrated part of the mobility ecosystem. As such, regulation focuses on restricting its impact, rather than encouraging its development and implementation in a way that maximizes overall mobility system benefits.

For example, in San Francisco, restrictive parking regulations forced BMW’s DriveNow to pull out of the city. Similarly, Car2Go’s 2018 car-sharing pilot was banned in 95% of Toronto’s residential areas. Local councils, which were responsible for the remaining 5% of residential areas, were allowed to ban Car2Go if they desired. Late in 2018, Car2Go, which claimed 80,000 users at the time, exited the market, citing parking fees and restrictions that made its service “inoperable.” Car sharing is still at an early stage in Singapore, but so far, car-sharing players face significant challenges, including high taxes on vehicle ownership, insufficient visible public-parking locations allocated for car sharing, insufficient promotion, and lack of integration with public transport.

Governments tend to set restrictions in a top-down fashion without adequate consultation with mobility service providers, users, or potentially affected businesses, leading to misunderstandings about how car-sharing schemes work. In Toronto, regulations were changed to shift from allocated parking lots to free-floating lots without adjusting for additional parking demand. This led to Car2Go racking up more than CAD $730,000 in parking fines.

Inadequate standards coordination between stakeholders in the mobility ecosystem can impact the overall effectiveness of car-sharing schemes. For example, there has long been a problem with lack of coordination between London boroughs around car sharing, leading to inconsistencies in rules regarding free-floating parking. This negatively impacted user experiences and caused difficulties for service providers operating across the city.

There are several common problems faced by car-sharing operators, including: (1) unsustainable business models, (2) unfavorable parking arrangements, and (3) lack of control over technology.

The main reasons car-sharing operators have struggled to achieve profitability are:

There are examples of profitable car-sharing operations. Often, these are local solutions limited in size and driven by differentiated use cases and/or business models. It is also worth mentioning asset-light models such as peer-to-peer, business-to-employee, and business-to-tenant models in which vehicles are owned by individuals or employers, as well as schemes subsidized by local/regional authorities (e.g., Citiz in France).

Adequate parking arrangements are critical to car-sharing schemes. Some countries or regions don’t allow free-floating car sharing, and suitable parking policies have not been defined in others. Several operators faced challenges due to limitations placed on their free-floating models; others experienced arbitrary bans to unclear regulations. Successful operations depend on making adequate parking arrangements with relevant authorities.

Operators must be digitally enabled from the start to have a viable car-sharing operation. Operators wholly reliant on third parties for system development encounter delays in making important changes to operating models as they learn more about the market. With the broader availability of third-party car-sharing operating software, the choice of provider is critical to the ability to scale the business across regions (e.g., to form interregional or multinational alliances).

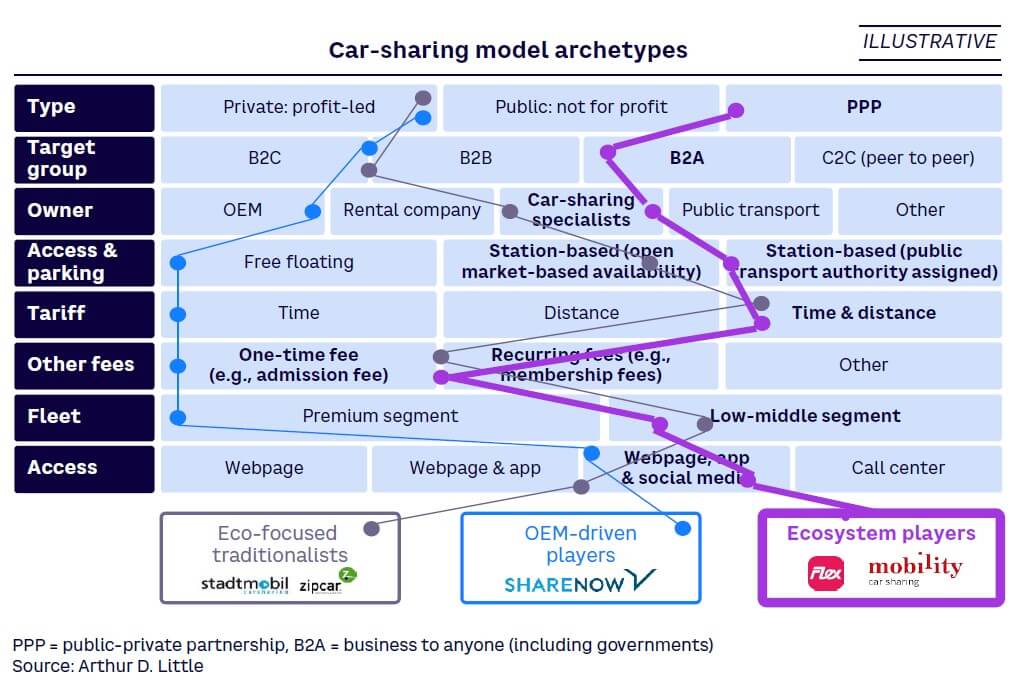

The ecosystem approach is the most evolved car-sharing model. In Figure 5, we see how its primary features compare to other models. In the ecosystem approach, car sharing is fully integrated with, and a contributor to, the overall mobility system. It’s designed to be user-centric and integrate with public transport via these key features:

In essence, the ecosystem approach seeks to align car sharing such that it improves mobility system performance and sustainability while enabling viable commercial operation. Below, we look at what this means for authorities and operators.

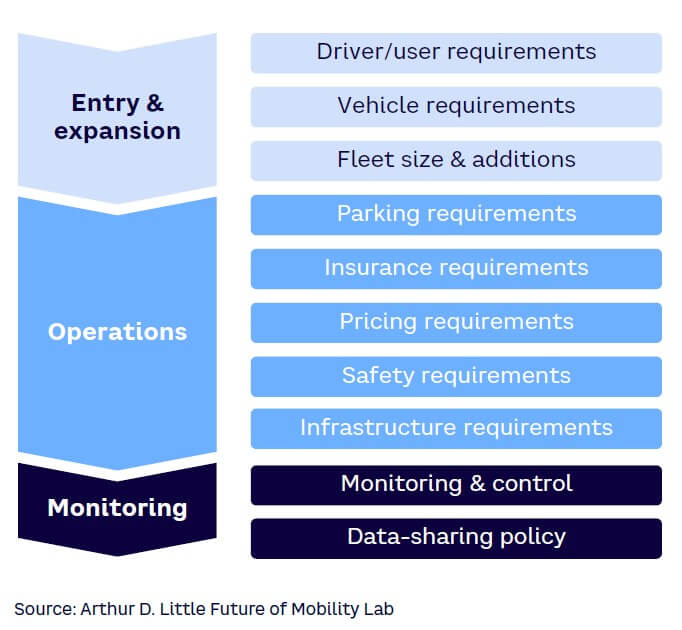

To create an ecosystem model that supports car sharing, city authorities and regulators should consider eight regulatory imperatives.

Cites and transport authorities have a wide range of parameters to consider in regulating car sharing (see Figure 6).

These parameters can be split conveniently into three categories:

Transport authorities should strike the right balance between "framing" and "enabling":

Inevitably, there are trade-offs between the various parameters and measures. For example, when setting parking requirements for car sharing, safety, security, environmental, and land-use concerns must be balanced with the financial viability of mobility operators and spin-off impacts for commercial businesses. All this must be done while remembering that a level playing field needs to be created to encourage competition. In general, cities and transport authorities have focused more on framing than enabling, and an ecosystem-based approach requires more attention to the latter. In striking a regulatory balance, the needs of the user/customer must be at the heart of all considerations.

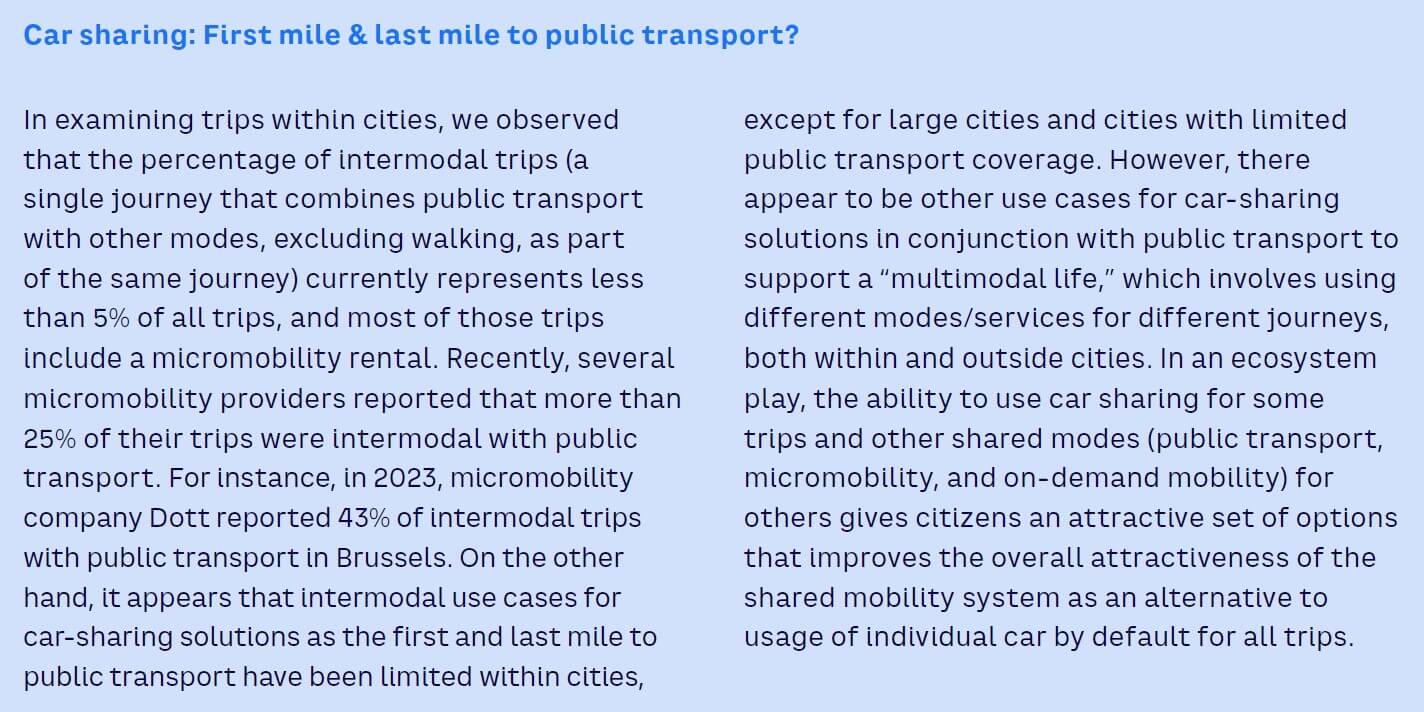

Mobility demand management measures for car sharing are important for optimizing the performance of the mobility system as a whole. As mentioned, when properly designed, car-sharing schemes can be a great complement to other mobility offerings in city centers and improve connectivity in city outskirts and rural areas, improving the overall attractiveness on the shared mobility system and providing an alternative to the use of private cars by default. Subsidies may be necessary to make servicing low-density areas commercially viable for the operator. Conversely, in some city centers, there may be a need to limit car sharing to avoid encouraging congestion and displacing mass transit ridership.

Demand management can also take the form of exemptions from parking, congestion, and/or toll charges (or discounts), helping to make car sharing more appealing than individual ownership.

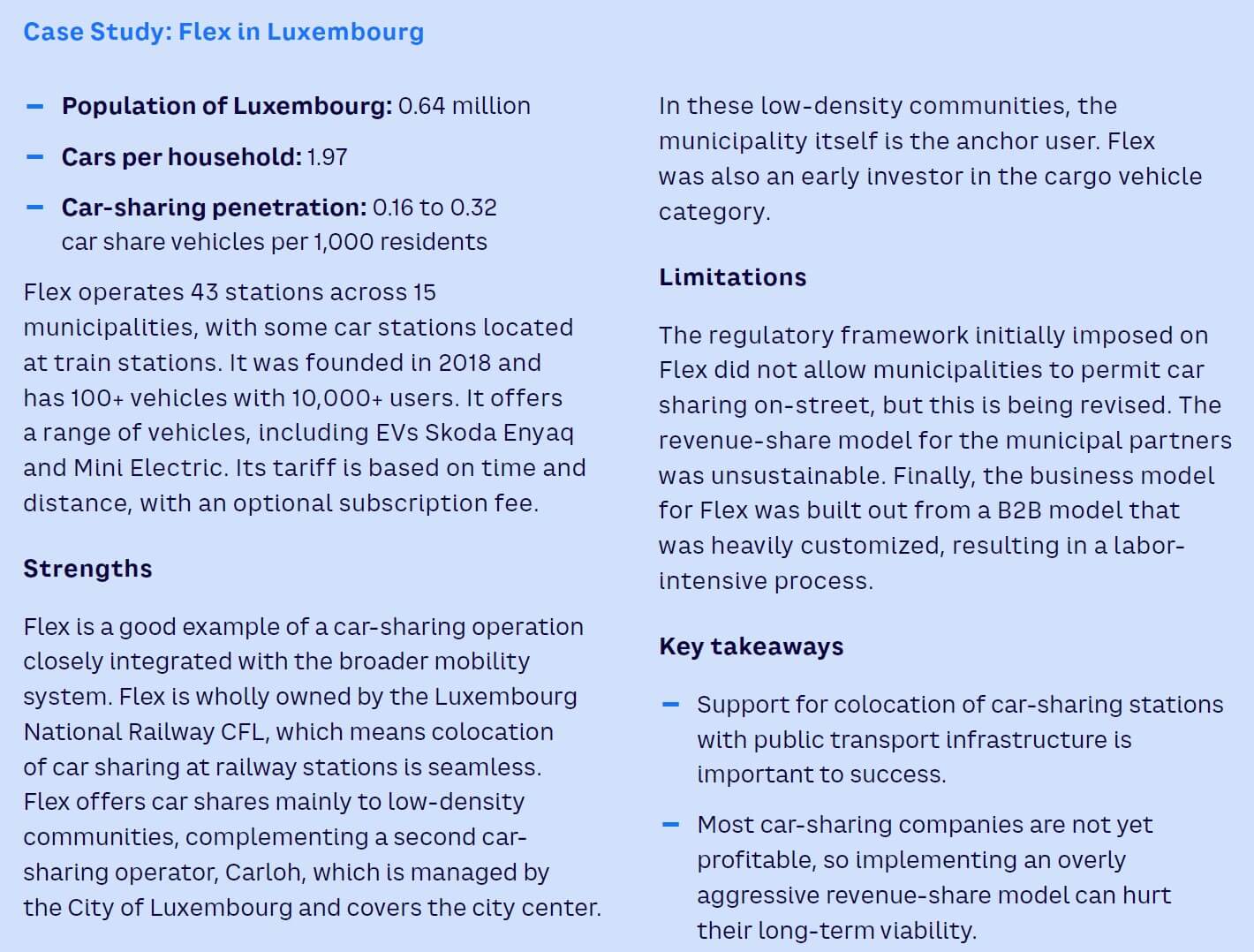

Infrastructure can help improve integration of various mobility solutions. For example, it can facilitate car-sharing stations being colocated with train, bus, or metro stations (refer back to case study “Flex in Luxembourg”). This is an excellent way to maximize car-sharing benefits.

Fostering close collaboration between new mobility service providers and public transport operators and authorities is important to help car share operations add value at the mobility system level. Authorities can help foster collaboration and innovation at the mobility system level through a range of measures:

Car-sharing schemes must achieve scale to be financially viable. Authorities and regulators should avoid restrictive regulations that dampen demand to the point that scaling becomes impossible.

Authorities should integrate the needs of car-sharing schemes into strategies for boosting penetration and adoption of EVs, especially provision of EV charging infrastructure, which is typically the primary bottleneck for the electrification of car sharing.

Whether primarily backed by public or private capital, car-sharing schemes can benefit from the involvement of public parties such as cities and transport authorities. This involvement can ensure good integration of the overall mobility system, especially when it comes to demand management. This includes evaluating direct or indirect forms of subsidies (e.g., access to parking, financial contribution according to metrics such as trip length, start/end in specific neighborhoods at specific times), especially taking into consideration that in many economies, the most heavily subsidized mode of transport, considered holistically, is the privately owned car.

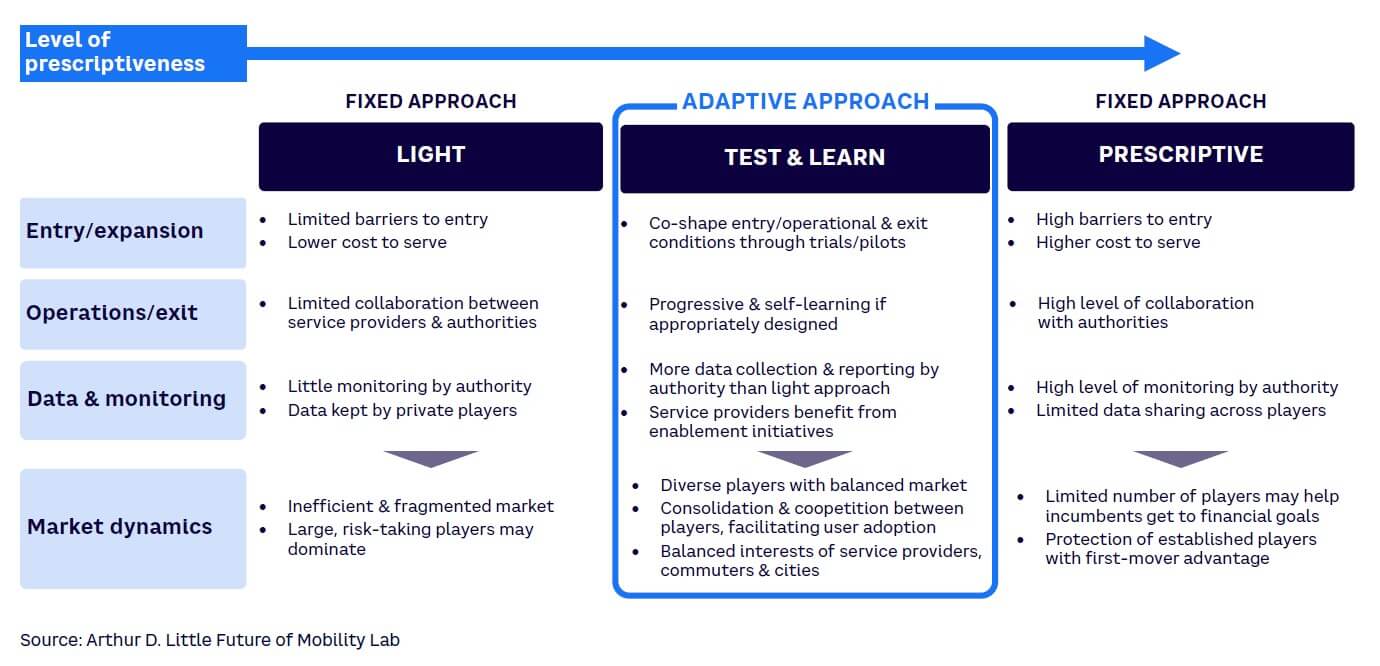

Experience shows that the most effective regulation follows a test-and-learn approach (see Figure 7).

Fixed approaches to regulation, whether light or prescriptive, have drawbacks. Light approaches can lead to a mobility market that is not as efficient as it could be and is difficult to control due to lack of data and effective enforcement levers. This often leads to market domination by larger players, who can absorb the most risk. Prescriptive approaches tend to have higher barriers to entry, high operating costs, less competition, and less innovation, although they protect the incumbents.

In between these extremes, a test-and-learn approach can deliver multiple benefits. Trials and pilots are an effective way to shape requirements in terms of entry, expansion, operations, and exit. However, short trials (less than three years) tend to be impractical due to the capital investment needed. Ideally, regulators should set conditions to encourage self-learning. In return for sharing more data, operators can benefit from the enabling measures described above.

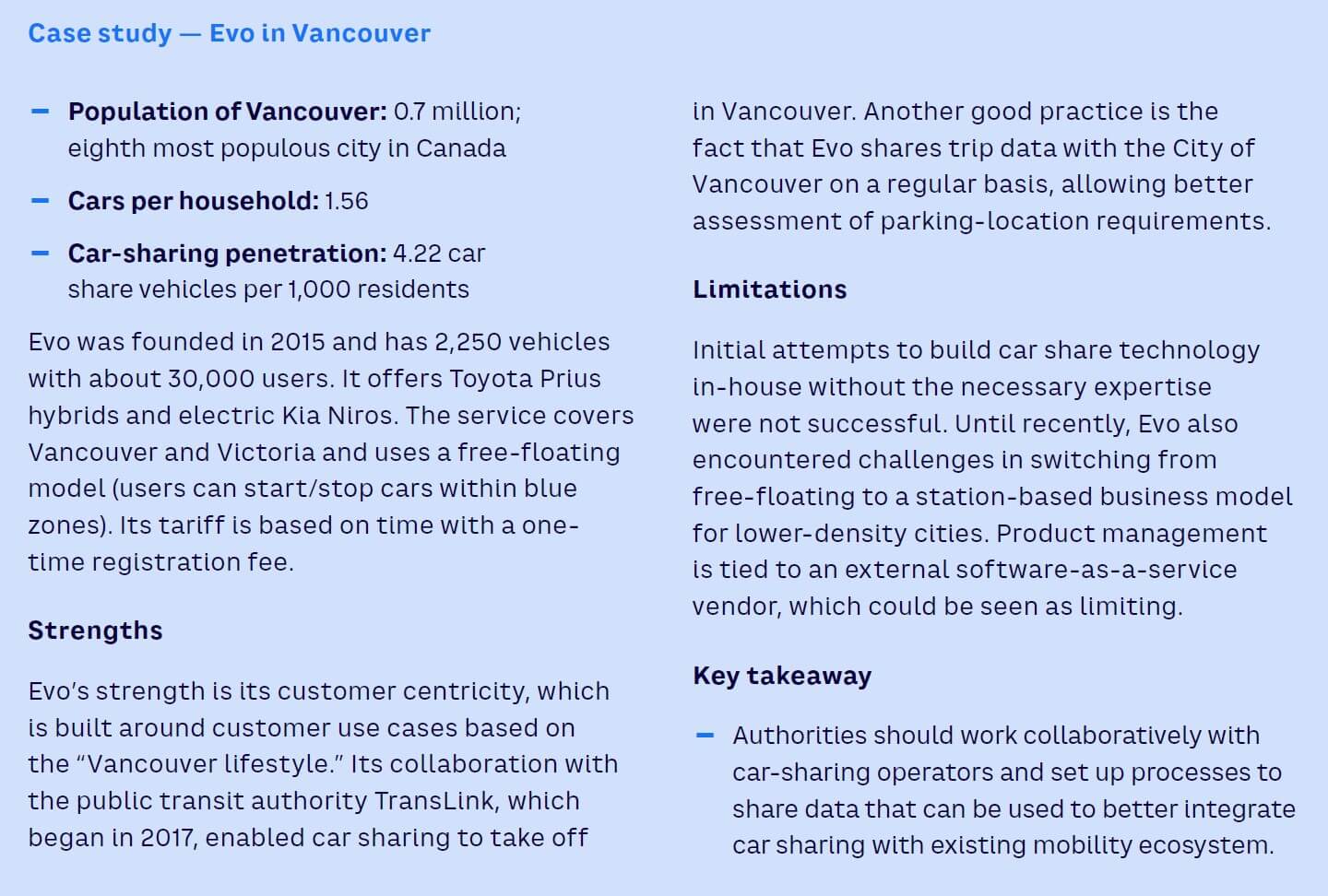

Done correctly, a test-and-learn approach leads to a more balanced market with a diverse set of players that balances the interests of all the actors in the system. Cooperation between players leads to closer integration and even consolidation, in most cases improving the attractiveness of the mobility offer and facilitating user adoption. This ideally results in predefined, close, consistent feedback loops and activities between regulators and operators. A good example of this approach is the way Vancouver cooperated with mobility operator Evo to help build an attractive, customer-centric offer (see case study “Evo in Vancouver”).

We can similarly identify a series of five key imperatives for success from an operator perspective.

With the active support of authorities, operators need to create customer-centric car-sharing schemes. This means avoiding a one-size-fits-all approach in favor of tailoring offerings to suit a variety of customer segments and behaviors. Customer needs differ greatly from city to city and from neighborhood to neighborhood within the same city, requiring careful analysis. Operators should carefully research the most attractive customer use cases and build communities of customers around these, as did Evo in Vancouver (see, again, case study “Evo in Vancouver”).

Collaboration with partners in the mobility ecosystem, especially authorities, is critical for achieving an outcome with mutual benefits. One of the most important considerations is data sharing, without which running an integrated mobility ecosystem is impossible. Although authorities have a key role in setting data-sharing standards and safeguards and providing suitable infrastructure, operators must cooperate and actively look for solutions that benefit multiple partners. Operators should work with authorities to help shape regulation, including being open to public/private partnerships.

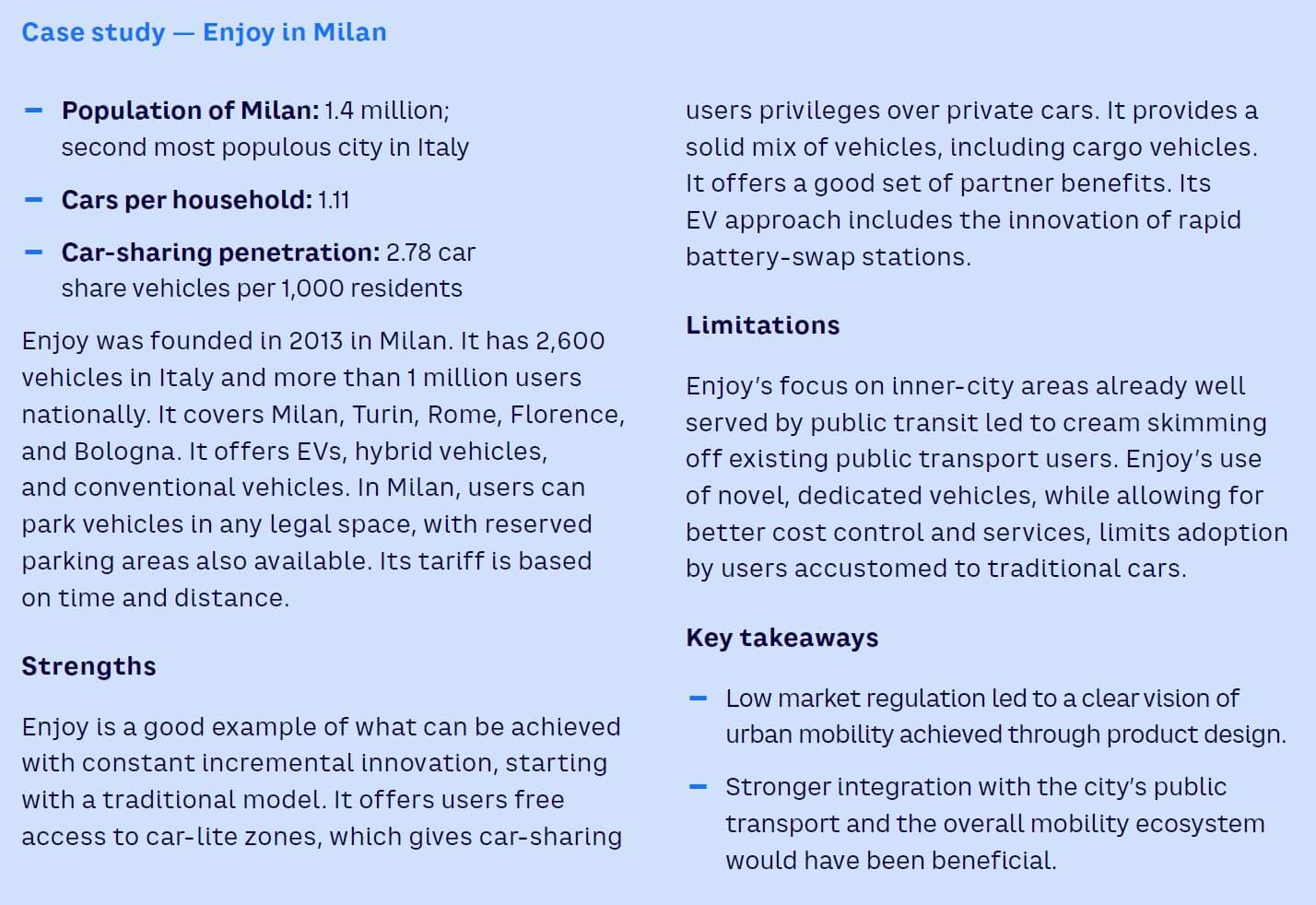

Operators must adopt a mindset of continuous innovation to grow scale and profit margin. Enjoy in Milan, which started with a traditional model, is a good example of what can be achieved with constant incremental innovation (see case study “Enjoy in Milan”). It offers users free access to car-lite zones, giving car-sharing users privileges over private cars, and it provides a solid mix of vehicles, including cargo vehicles. It also offers a good set of partner benefits and rapid battery-swap stations for EVs.

Car-sharing businesses that only focus on one segment tend to be more difficult to scale and may not be commercially viable (see case study “Share Now in Berlin”). From an overall ecosystem perspective, such schemes are usually suboptimal because they are hard to integrate with other mobility modes. Scalability requires aiming at the broadest possible customer population (whether consumer, business, or government) with careful customer segmentation and profiling to ensure customer-centric offerings.

Car-sharing operators must consider the overall mobility system, rather than focusing solely on the performance of their operation. Indeed, an ecosystem-based approach is much more likely to lead to sustainable operations in the long run, as the greater overall value provided to consumers is matched with a higher willingness to pay for the service.

Car sharing has a checkered history in many cities, with a few successes and some notable failures. But as the shift away from “car ownership by default” continues and new mobility offers become better integrated into the overall mobility system, car sharing has the potential to come into its own and deliver major benefits to both customers and transit authorities. Car sharing is even more attractive as an individual mobility solution when paired with the shift to EVs, and as AVs and robotaxis become mainstream, we may see car sharing increasingly converge with ride sharing.

The key to success for all stakeholders (transit authorities, operators, investors, and suppliers) is adopting an ecosystem-based approach. Car sharing benefits from being fully integrated with, and contributes to, the overall mobility system, especially public transport; this also benefits citizens.

For city and transport authorities, this means finding the right balance between framing and enabling regulations and actions, actively managing car-sharing demand for the benefit of the overall system, setting conditions that enable close collaboration between players, enabling data sharing, fostering innovation, and integrating physical infrastructure. In many places, subsidies can be justified by the resulting reduction in privately owned cars.

Operators must become and remain customer-centric, acting local, target the broadest possible customer population, be willing to collaborate and share data with others, take a broad system perspective, and constantly innovate.

With this approach, car sharing has the potential to become a key part of a sustainable mobility future for our cities and regions.

Notes

[1] Trip chaining is a travel pattern involving multiple small, interconnected trips.

[2] “Car Club Annual Report: United Kingdom.” CoMoUK, 2021.

[3] Nicholas, Michael, and Marie Rajon Bernard. “Success Factors for Electric Carsharing.” International Council on Clean Transportation (ICCT), Working Paper 2021-30, August 2021.

[4] In addition to varying between user types, the economics of car sharing versus ownership vary between markets, based on issues such as taxes and incentives.

[5] Van Audenhove, François-Joseph, et al. “The Future of Urban Mobility 2.0 – Imperatives to Shape Extended Mobility Ecosystems of Tomorrow.” Arthur D. Little/UITP, January 2014.

cloud technology

A través de su vehículo A&G Real Estate Sustainable Developments SIC...