Empowered by technology and in line with customers’ digital habits, demand-responsive transport (DRT) is extending shared-mobility coverage and optimizing public transit. In this Viewpoint, we examine the extent to which DRT can help public transport authorities (PTAs) and public transport operators (PTOs) build more sustainable, resilient, and human-centric mobility systems.

As PTOs look for ways to maximize the attractiveness and efficiency of shared mobility systems[1] and transition toward net zero, DRT is moving to the forefront. On-demand transport services have been part of public transport, but in a limited way:

The first DRT schemes resulted in more questions than answers. Adoption and pooling rates were low, drivers’ paths had to be manually mapped each morning, and costs were high (euros spent per passenger-kilometer [PAX-km][2]) for the PTAs and PTOs that launched the initiatives.

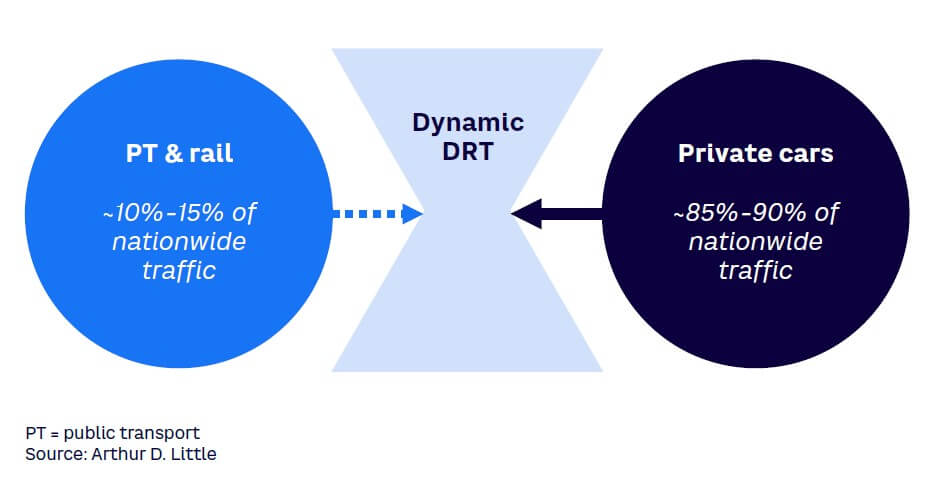

In a 2020 Viewpoint (see “Rethinking On-Demand Mobility”), Arthur D. Little (ADL) examined on-demand solutions more broadly and concluded that the success of such services would “depend on the ability of public transit operators to develop the required levels of agility to run services which are, by definition, less predictable than their historical offerings.” Now, on-demand mobility is more mature, and there is segmentation between private services (ride hailing) and public services (DRT) — see Figure 1. However, DRT has remained a niche market and lacks integration into global mobility strategies. Four years ago, at the genesis of DRT, we raised several questions in that Viewpoint; the main question was the extent to which on-demand could complement or replace public transit. Both have been attempted over the past few years, with mixed results.

That Viewpoint also concluded that:

“On-demand solutions may well prove to be harmonious complementary services to public transit and, in some cases, replace fixed-route/fixed-schedule services, provided there is a business case based on accurate demand planning and sound cost-benefit analysis. However, the extent to which these solutions will be operated by private and public players in the future is still to be defined. The answer will depend on the ability of public transit operators to develop the required levels of agility to run services which are, by definition, less predictable than their historical offerings. It will also depend on whether private players can achieve the appropriate level of flexibility as they work with a number of different stakeholders, developing services to address the public interest at large. That said, we have no hesitation in recommending that operators experiment further as they assess the opportunities in on-demand public transit.”

What has happened since we wrote those lines four years ago? On-demand transport is mutating as the result of the following:

Today, there are three key questions to consider:

Based on expert views and market analysis completed by ADL’s Mobility Competence Center, we estimate there have been ~1,400 DRT projects initiated around the globe, with close to 1,000 still active. We continue to observe an increase in the number of DRT projects. ADL has gathered valuable insights on DRT, including:

Public transport requires high volumes of passengers to be efficient, and DRT enables expansion to both low-density areas (peri-urban and rural) and in low-demand situations (nights, weekends, holidays, suburb-to-suburb journeys, and other specific origin-to-destination journeys).

DRT has been introduced in many cities and territories as a way to:

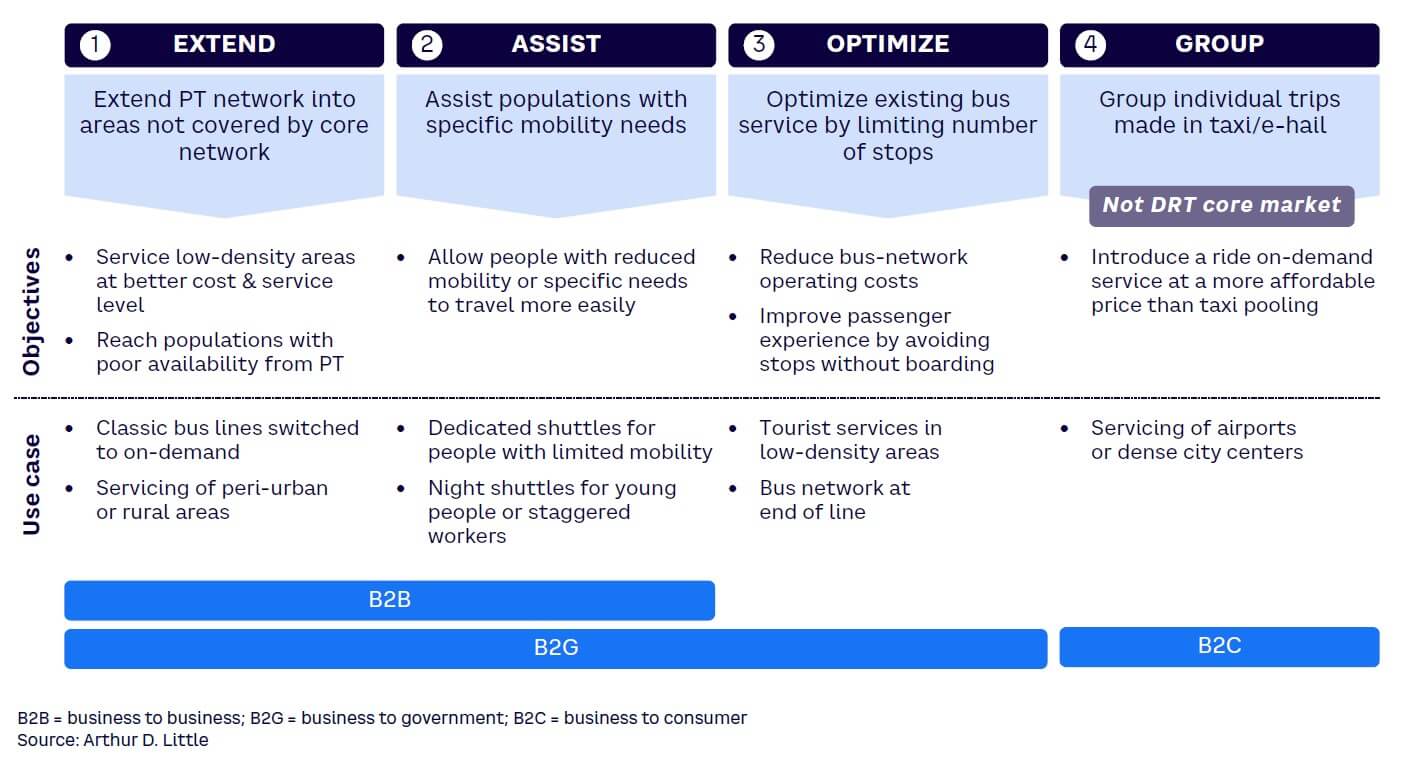

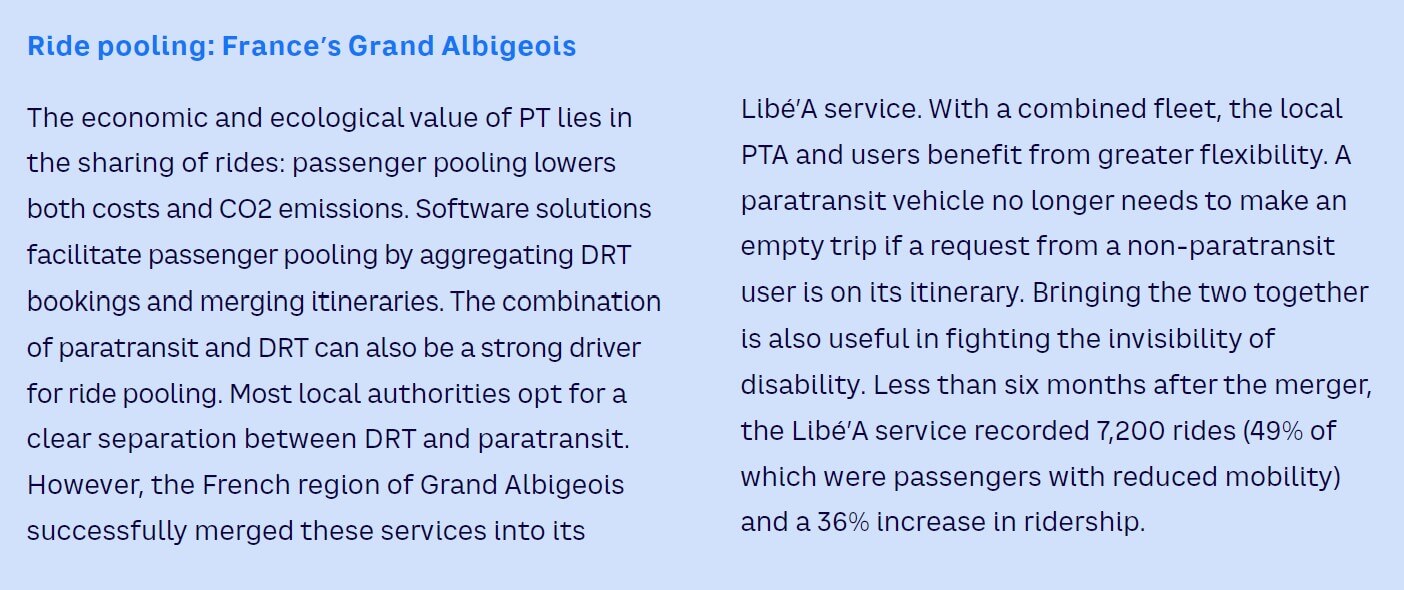

DRTs cannot successfully serve all these customers simultaneously, so PTAs must focus on a few use cases (see Figure 2). Some PTAs have successfully implemented separate DRT services in the same geographic area, such as a paratransit service during the day and night bus service for young people.

Transit systems are generally sized to absorb peak-hour riders; the fact that DRT systems have no peak hours means its resources (e.g., buses and employees) are better used throughout the day. It may also allow DRT operators to use PT vehicles that usually sit idle during non-peak hours.

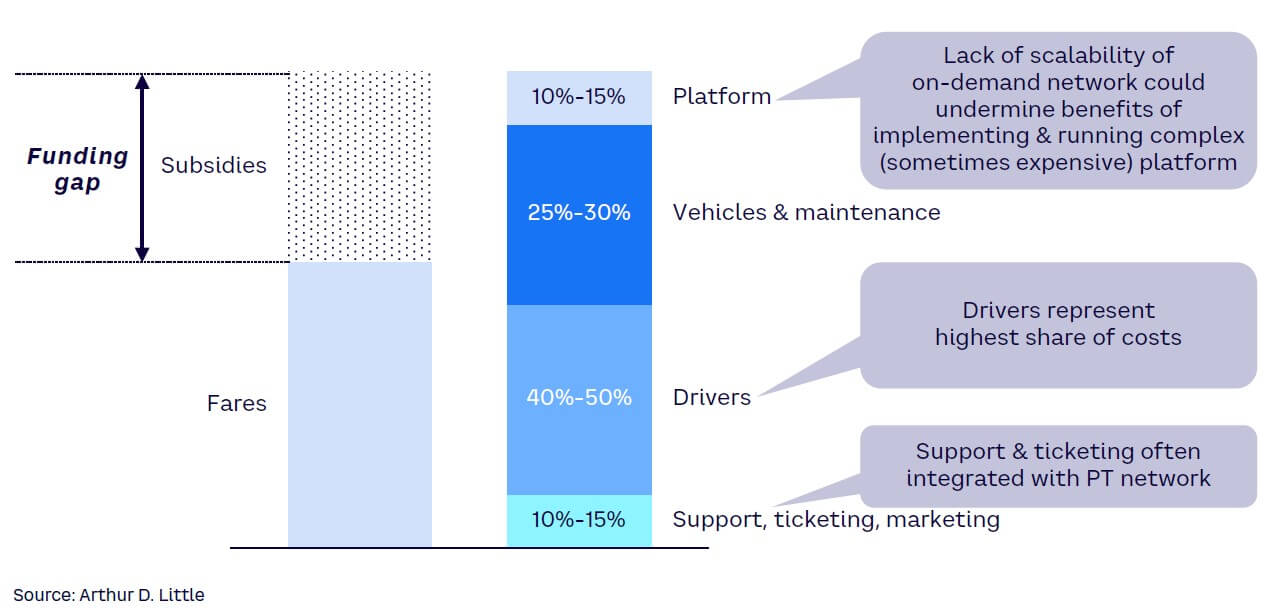

When discussing financial viability, it is important to first debunk the idea that on-demand transportation services can be profitable. Except in the case of shared taxi rides, DRT follows the traditional financing model of public transportation in most of the world, which includes subsidies.

On average, DRT services only generate a cost-coverage rate of between 5% and 15% (depending on the networks) compared to 15% to 40% for traditional bus services (see Figure 3). Even relatively high fares do not cover the costs of the service. It is therefore necessary to include it in the PT financing scheme and leverage the five success factors discussed below.

A DRT implementation must have clear objectives and take a customer-centric approach. As discussed, DRT is not a one-size-fits-all solution. Rather, it’s a targeted response to specific transportation challenges, including optimizing existing on-demand offerings, expanding service coverage, partially replacing a bus network, and/or facilitating the grouping of individual trips.

PTAs should consider conducting both in-house and external analyses to assess DRT’s potential in their area and identify success factors with an eye toward creating seamless journeys that address passenger concerns before initiating service. Note that preliminary analyses on both strategic and operational aspects have a better ROI than a quick go-to-market without studies.

There are four major pillars to consider when defining objectives:

DRT services can be operated using various models (see Figure 4). Each DRT model has advantages and disadvantages. Although certain models are specifically tailored to meet user requirements (e.g., door-to-door services for disabled persons), most universal on-demand services take one of these app

cloud technology axon

Founded by professionals with expertise in breastfeeding, engineering ...